South America Data Center Market 2025-2030 – ESG, Renewable Energy, and Growth Trends Illustrated with Wind Turbines, Solar Panels, and Server Infrastructure. Image Credits: Kencrave

13 min read

Business

Esg, Growth, And Renewable Power: South America Data Center Market Analysis 2025 2030

Renewable Energy, Green Financing, and Market Impact in South America

Executive Summary

South America is rapidly emerging as one of the world’s fastest-growing data center markets. Once overshadowed by established global hubs such as Frankfurt, Northern Virginia, and Singapore, the region is now attracting large-scale investment driven by cloud adoption, hyperscaler expansion, regulatory localization, and abundant renewable energy.

The South American data center market is projected to grow from USD 3.78 billion in 2025 to USD 6.42 billion by 2030, representing a compound annual growth rate (CAGR) of 11.18% (Mordor Intelligence, 2025).

IT load capacity is expected to expand from 1.51 GW to 2.23 GW over the same period, reflecting rising demand from hyperscale cloud platforms, AI workloads, and 5G-enabled edge computing.

Brazil and Chile anchor the region’s growth. Brazil leads in scale and capacity, while Chile has positioned itself as the region’s sustainability-focused hub, attracting ESG-driven hyperscaler investment.

Together, these markets illustrate how renewable energy availability, green financing, and regulatory clarity are shaping South America’s data infrastructure landscape.

South America's renewable energy growth, green financing, and data center market impact, highlighting Brazil and Chile’s energy mix, ESG investment trends, cloud demand, and internet expansion.

The Forces Driving South America’s Data Centre Growth

The surge is driven by concurrent trends that have created unprecedented demand for local data infrastructure.

Connected Population: With an estimated 345 million internet users in South America as of October 2025 anda young population, the continent offers great potential for digital services (ITU Internet Use Statistics , World Population Review 2025). Colombia’s creative industries and São Paulo’s fintech are driving demand for low-latency data services.

Subsea Cable Expansion: South America’s digital links to the world are strengthening. High-capacity subsea cables such as Humboldt, Firmina, and Malbec now connect the region to global data routes.

Cities such as Chile, Brazil, and Argentina are the landing points. They are turning into key network hubs that enable faster connections and support the growth of data centres.

Data Sovereignty Regulations: Regulation is now a growth driver. Modeled on Europe’s GDPR, Brazil’s Lei Geral de Proteção de Dados (LGPD) enforces data protection and localisation rules. Similar laws are being set in other South American Countries, forcing businesses to host and process user data locally, driving strong demand for regional data centers.

Post-Pandemic Digital Economy: The COVID-19 pandemic altered the digital landscape. There was a 30% increase in internet usage in Latin America, boosting remote work, e-commerce, and fintech growth (World Bank). This shift has created a demand for stronger local computing power.

Hyperscalers Race for Cloud Market Dominance: Competition among major cloud providers, AWS, Google Cloud, and Microsoft Azure, is fueling infrastructure growth.

These cloud providers are the largest consumers of capacity. They are expanding regional networks that meet enterprise needs. Microsoft’s $3.1 billion investment in Cloud and AI highlights the scale of this shift.

Key Markets: Brazil, Chile, and Emerging Hubs Brazil: Scale and Renewable Advantage

Brazil is also the region’s renewable energy leader. Around 89% of its electricity comes from renewables, largely hydropower, supported by fast-growing wind and solar capacity. This gives Brazil a structural advantage in powering large-scale data infrastructure with low-carbon electricity.

Brazil accounts for approximately 40% of Latin America’s data centre capacity. São Paulo ranks among the world’s top emerging data centre markets. The country’s scale, dense fibre networks, and steady enterprise demand keep it in a leadership position. Demand comes from both traditional enterprise clients and fast-growing AI and IoT workloads.

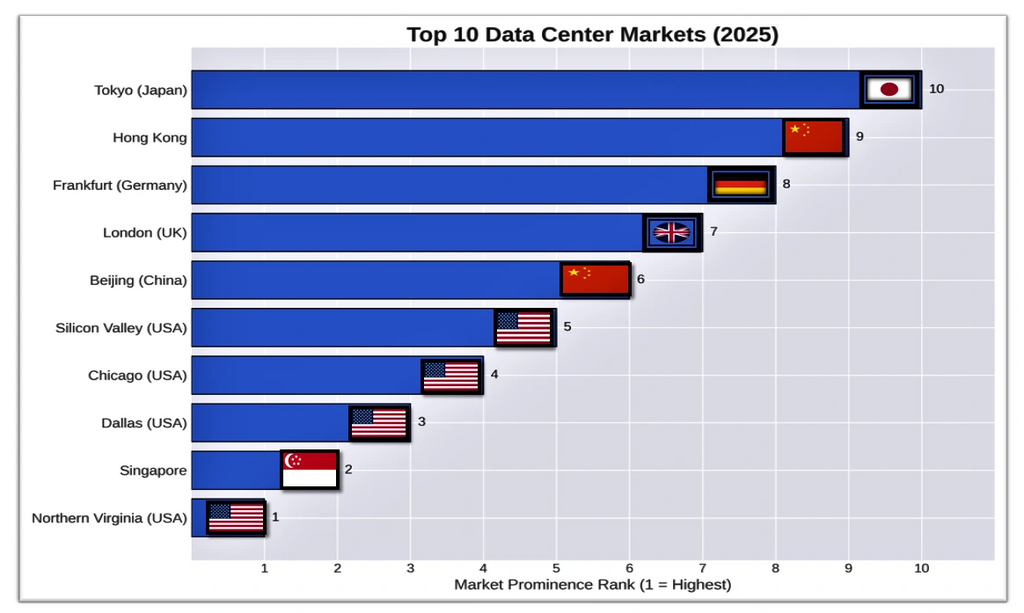

Top 10 Global Data Center Markets 2025 ranked by prominence with country flags – Northern Virginia, Singapore, Dallas, Chicago, Silicon Valley, Beijing, London, Frankfurt, Hong Kong, Tokyo. Source: Abramwireless

Prominence indicates how influencial, important and dominant a data center market is globally.

Key Indicators of Prominence

Total capacity (MW): How much IT load the market can support.

Hyperscale presence: Number of major cloud providers (like AWS, Azure, Google Cloud).

Connectivity: Access to fiber networks, internet exchanges, and latency performance.

Investment volume: Real estate, infrastructure, and energy investments.

Strategic location: Proximity to financial hubs, population centers, or geopolitical importance.

Regulatory and sustainability leadership: Compliance with data laws and green energy adoption.

Takeaway: The graph highlights that while the U.S. remains dominant, Asia-Pacific and Europe are catching up fast, driven by AI adoption, sovereign data laws, and sustainability mandates.

Chile: The Sustainability-Focused Hub Chile has positioned itself as the region’s sustainability-focused data centre hub. In 2024, renewables supplied about 70% of Chile’s electricity, driven mainly by rapid growth in solar and wind. While this share is lower than Brazil’s hydro-led mix, Chile’s energy transition is among the fastest in Latin America.

Chile is the first Latin American country to legally commit tocarbon neutrality by 2050. It is phasing out coal generation by 2040 and has issued green bonds while enforcing a national CO₂ tax to accelerate clean energy investment.

These policies, combined with political stability, make the country highly attractive to hyperscalers with Environmental, Social, and Governance mandates.

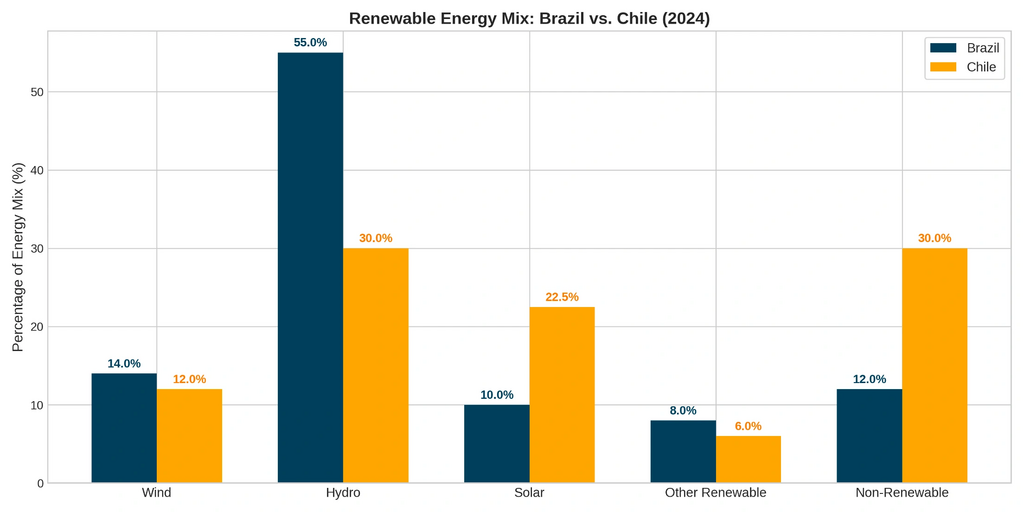

Brazil vs Chile renewable energy mix 2024 bar chart comparing hydro, wind, solar, other renewables, and non-renewable sources

Key Insights from the Renewable Brazil's and Chile's Energy Mix

Brazil's grid is powered primarily by hydropower (55%), giving it a stable, low-carbon foundation for data center growth, though with some climate vulnerability.

Chile leads in solar penetration (22.5% vs Brazil's 10%), reflecting its aggressive energy transition and making it ideal for sustainable data operations aligned with corporate ESG goals.

Brazil's higher overall renewable percentage (89% vs 70%) provides an immediate carbon advantage, while Chile's diversified mix signals faster transition momentum, with both countries offering strong green power propositions for data center operators.

Implications: High renewable penetration lowers operating costs and carbon intensity, positioning South America favorably against fossil fuel-dependent digital infrastructure regions.

Emerging South American Data Center Markets Beyond Brazil and Chile, several countries are rapidly expanding their data center presence due to digital growth, supportive policies, and rising demand for cloud and AI infrastructure:

Colombia: Experiencing strong growth, attracting major AI infrastructure investments backed by national strategies.

Peru: Smaller in capacity but actively participating in regional expansion.

Panama: Developing as a digital hub, seeing increasing data center investment alongside Costa Rica and Peru.

Argentina: Drawing investment with energy opportunities from resources like the Vaca Muerta shale play.

Uruguay: Leveraging renewable energy to support sustainable data center development.

ESG Leadership and Global Operators

Global data center and cloud operators are reinforcing ESG leadership across the South American region:

Equinix sources 96% renewable energy globally and targets climate neutrality by 2030 through PPAs and advanced cooling systems.

Google has matched 100% of its electricity consumption with renewables since 2017 and is pursuing 24/7 carbon-free energy by 2030, with average data center PUE of 1.09.

Microsoft aims to be carbon negative by 2030, deploying waste-heat recovery and circular hardware reuse strategies. Its decision to establish a major Azure region in Chile underscores the country’s growing role as South America’s green data center hub.

Brazil remains the regional hub, with major investments in São Paulo, while Chile is emerging as a sustainability-focused destination due to its fast-growing wind and solar capacity.

Hyperscalers like AWS, Google, and Microsoft set the standard for ESG alignment, encouraging local operators to adopt global sustainability practices.

Green financing, advanced cooling technologies, and strategic renewable energy agreements are key trends driving growth and ensuring that South America’s data center market expands responsibly and sustainably.

The Market Players

There are three tiers of players that pose competition, which pushes the market to grow and innovate faster.

Global Colocation Giants: Companies such as Digital Realty, Equinix, and EdgeConnex form South America’s digital infrastructure backbone. These global colocation giants operate interconnected hubs that support enterprises and small cloud providers to ensure strong network resilience and connectivity.

The Hyperscalers: AWS, Microsoft Azure, and Google Cloud are considered to be the demand drivers. Their capital expenditure on large data centers defines scale and expansion across the region.

Regional Champions: Regional companies such as KIO Networks, Elea Digital, and ODATA drive growth through local insight. Their local expertise on regional markets helps them secure land, permits, and power faster than global competitors.

The Role of Green Financing

The growth of sustainable data centers is being catalyzed by specialized financing. Green bonds, sustainability-linked loans (SLLs), and financing from development banks (e.g., IFC, IDB Invest) are becoming critical tools. These instruments tie funding to ESG performance targets, such as achieving a specific Power Usage Effectiveness (PUE) or renewable energy percentage.

Regional operators like Scala and ODATA have successfully tapped these markets to fund expansions, demonstrating how global ESG capital flows are directly enabling South America's infrastructure build-out.

Challenges Ahead

The data center market’s rapid growth in South America has exposed structural and operational challenges that need to be considered.

Geopolitical and Economic Volatility: Brazil’s currency, the Brazilian real (BRL), is a characteristically volatile emerging market currency, sensitive to global commodity prices and domestic politics.

This inherent volatility exposes businesses to substantial FX risk, with direct implications for capex costs, power contracts, and foreign debt exposure. In 2024, the BRL lost more than 20% of its value against the USD, before appreciating roughly 13% year-to-date in 2025 due to high domestic interest rates and a weaker US dollar.

Power and Water Scarcity: In South America, Brazil, Chile, and Colombia are driving data center growth while prioritizing sustainability. Brazil hosts major operators like Scala Data Centers and ODATA, which integrate 100% renewable energy and liquid cooling to support AI workloads.

Chile is expanding its green data center regions, leveraging wind and solar energy. Colombia is rapidly scaling its infrastructure with a focus on renewables.

Talent and Supply Chain: Shortages of skilled technical workers and constrained supply of critical equipment, such as switchgear and generators, continue to slow expansion. In early 2024, Brazil delayed about 5.39 GW of planned power generation capacity, according to the National Electric Energy Agency (ANEEL).

Delays affected solar (2.64 GW), wind (1.95 GW), biomass (412 MW), and other projects. Causes included construction issues, licensing delays, grid access bottlenecks, PPA challenges, and regulatory uncertainty.

Outlook: Distributed, AI-Ready, and Sustainable

The next phase of growth is shifting away from centralized hyperscale facilities toward more distributed infrastructure.

Sustainability as a License to Operate: 24/7 carbon-free energy sourcing and green building standards will evolve from a market differentiator to a basic requirement for new data center projects that are driven by both future regulations and corporate ESG.

The Edge Computing Wave: Real-time applications such as telemedicine, autonomous mining, and smart cities will drive the rise of smaller edge data centers in secondary cities, positioning computing power close to users for lower latency and faster processing.

AI-Ready Infrastructure: The global AI surge will require a new generation of data centers in South America. These facilities will be equipped with high-power density and direct liquid cooling to support AI training workloads. Forward-thinking developers will gain a strong competitive edge.

Building South America’s Digital Foundation

South America’s data boom is more than infrastructure growth; it's the continent's foundational bedrock for its own digital independence. Investing billions in local computing capacity will reduce its reliance on foreign infrastructure, which will foster local innovation and strengthen global competitiveness. With every new data center, South America’s data infrastructure grows more resilient, faster, and stronger.

Implications for Stakeholders

1. Policymakers: Develop clear regulatory frameworks that encourage sustainable data center growth. Offer incentives such as tax breaks and renewable energy subsidies, while ensuring data sovereignty policies balance privacy with investment appeal.

Support workforce development through technical education and training programs to build local expertise for operating advanced AI and cloud infrastructure. Facilitate streamlined permitting and licensing to reduce project delays and attract both domestic and international investors.

2. Corporations and Data Center Operators: Focus on integrating renewable energy through Power Purchase Agreements (PPAs) and local green energy partnerships. Implement advanced cooling technologies, including liquid immersion systems, to increase efficiency and reduce water usage.

Align ESG strategies with international standards such as LEED and ISO 50001 to attract hyperscaler clients and investors. Expand AI-ready infrastructure with scalable, high-density power solutions to meet growing demand from cloud and edge computing applications.

3. Technology and Cloud Companies: Lead the market in carbon neutrality, renewable energy adoption, and resource efficiency to influence local operators and policy frameworks. Partner with governments and regional operators to develop resilient, distributed infrastructure that reduces latency and strengthens digital independence.

Invest in edge computing, AI-ready data centers, and initiatives supporting data sovereignty to meet the demands of fintech, telemedicine, smart cities, and other emerging digital applications.

Key Takeaways

South America is the fastest-growing data center market in 2025, fueled by cloud demand, AI, and post-pandemic digitalization.

Brazil leads in capacity; Chile leads in sustainability. Emerging markets like Colombia, Peru, Panama, Argentina, and Uruguay are rapidly expanding.

Renewable energy and advanced cooling are central to sustainable growth.

The market faces challenges in economics, resources, and talent.

Growth will focus on distributed, AI-ready, and edge infrastructure.

Collaboration between governments, corporates, and tech companies is key to resilient, inclusive digital development.

Frequently Asked Questions

1. Why is South America the fastest-growing data center market?

South America is growing fastest due to cloud and AI demand, data-localization laws, subsea cables, and abundant renewable energy.

2. Which South American country is best for hyperscale data centers?

Brazil leads in scale and connectivity, while Chile leads in renewable energy, ESG policy, and sustainability-focused hyperscale deployments.

3. How important is renewable energy for data centers in South America?

Renewables are critical: Brazil runs on an estiamated 89% clean energy and Chile 70% estimate, lowering costs, emissions, and ESG risk for hyperscalers.

4 . Are hyperscalers investing in South America?

Yes. AWS, Google, and Microsoft are investing billions in South America to support cloud, AI, data sovereignty, and low-carbon operations.

5. What challenges affect data center expansion in South America?

Key risks include power and water constraints, FX volatility, talent shortages, and grid connection delays despite strong demand.

.png)