Foreign Direct Investment (FDI) has long been a cornerstone of Europe’s economic growth, job creation, and technological progress. FDI typically involves long-term strategic commitments, such as acquiring at least 10% of voting shares in a foreign enterprise. It's important to note that the cited EY survey data measures FDI projects, which include new physical operations like manufacturing plants and R&D centers, capturing the broader trend of investment commitments.

Key Takeaway: Europe’s decline in foreign direct investment is not cyclical, it reflects a structural loss of competitiveness driven by geopolitical risk, regulatory complexity, and stronger industrial incentives in rival economies.

Yet Europe’s investment climate has shifted sharply. According to the EY Europe Attractiveness Survey (2025), Europe recorded its lowest number of FDI projects in nine years during the 2024–2025 period. This decline signals a structural change in global investment patterns and raises urgent questions about Europe’s competitiveness.

FDI projects in Europe 2015 to 2025 line graph showing record peak in 2017, post‑pandemic surge, and projected structural decline to 2024 low.

While part of the downturn reflects a broader global slowdown in capital expenditure following the post-pandemic surge, the scale and persistence of Europe’s decline suggest deeper issues tied to geopolitics, regulation, and industrial strategy. This trend is particularly acute for Europe, as investment flows are increasingly re-concentrating in North America and East Asia.

Causes of Europe’s FDI Decline: Geopolitics, Regulation, and Energy Costs

Geopolitical instability has become a major deterrent for foreign investors. The ongoing Russia–Ukraine war has elevated risk perceptions across the continent, particularly in Central and Eastern Europe. Trade uncertainty and political risk have weakened investor confidence throughout the region.

Regulatory complexity has constrained Europe’s appeal. In February 2025, EU officials acknowledged that excessive administrative and sustainability-related requirements were limiting competitiveness, prompting renewed discussions on regulatory reform.

While environmental standards are a core European value, slow permitting processes, fragmented national rules, and overlapping reporting obligations raise project costs and extend timelines, critical factors for multinational investors deciding where to locate new facilities.

High energy prices compound these challenges. Compared to the United States and parts of Asia, European manufacturers face structurally higher electricity and gas costs, reducing margins and long-term predictability. For example, industrial electricity prices in key economies like Germany have remained multiples of those in the U.S., driven by geopolitical supply shifts and network costs.

Structural Competitiveness and Manufacturing Shifts

Europe’s FDI decline reflects deeper structural competitiveness issues. Relative to the United States and China, Europe struggles with:

Slower industrial scaling.

Fragmented industrial policy across member states.

Smaller, less integrated capital markets.

EY reports a sharp fall in manufacturing investment in 2024, as capital increasingly flows toward the U.S. and China. The U.S. Inflation Reduction Act and CHIPS Act provide large, clear fiscal incentives, while China offers scale, speed, and tightly integrated supply chains. These environments reduce uncertainty and accelerate returns as decisive advantages for global firms.

Europe’s policy response, by contrast, remains uneven. National subsidy regimes differ widely, and cross-border projects still face legal and bureaucratic friction within the single market.

FDI inflows comparison chart Europe United States China 2020 to 2025 showing investment trends and projections.

Key Insightsfrom the Actual FDI Inflows: Europe vs. United States vs. China (2020–2025) Europe

Highly volatile flows: from $151B in 2021 to –$106B in 2022 (a net outflow).

Weak recovery: only $16B in 2023, then estimated $182B in 2024 and projected $170B in 2025.

This volatility reflects financial conduit flows (e.g., Luxembourg), making Europe less stable for FDI.

United States

Consistently strong inflows: peaked at $388B in 2021, then stabilized around $285–343B.

Projected to remain the global leader with $330B in 2025, showing resilience and investor confidence.

China

Moderate but steady inflows: $144B in 2020 → $189B in 2022, then declining to $115B (2024 est.) and$108B (2025 proj.).

Reflects reduced green financial FDI and policy-driven shifts, though still significant in scale.

Strategic Implications

Investor Confidence: The U.S. remains the most attractive destination due to policy stability and strong market fundamentals, reinforcing its role as the global FDI hub.

Europe’s Challenge: Persistent volatility undermines investor trust, signaling the need for structural reforms, reduced reliance on financial conduit flows, and stronger strategic autonomy.

China’s Shift: Declining inflows highlight the impact of geopolitical tensions and reduced green finance, pushing China to diversify supply chains and recalibrate its investment model.

Global Capital Reallocation: Investors are increasingly de‑risking by redirecting funds toward stable, policy‑backed markets (U.S.) and emerging hubs in Asia, reshaping the global investment landscape.

Takeaway: FDI flows are realigning toward stability and strategic industries, leaving Europe at risk of marginalization unless it adapts.

Regional Fragmentation of FDI in Europe

The downturn in foreign investment in Europe is not uniform. Central, Eastern, and Southeastern Europe have suffered the steepest declines. According to data cited by EY, total inflows to these regions fell by roughly 25% in 2024. Poland alone experienced a 48% drop.

These disparities reflect:

Higher exposure to geopolitical risk.

Weaker infrastructure in some regions.

Lower fiscal capacity to match U.S.-style incentives.

The result is a widening investment gap between Europe’s core economies and its periphery, threatening long-term convergence within the EU.

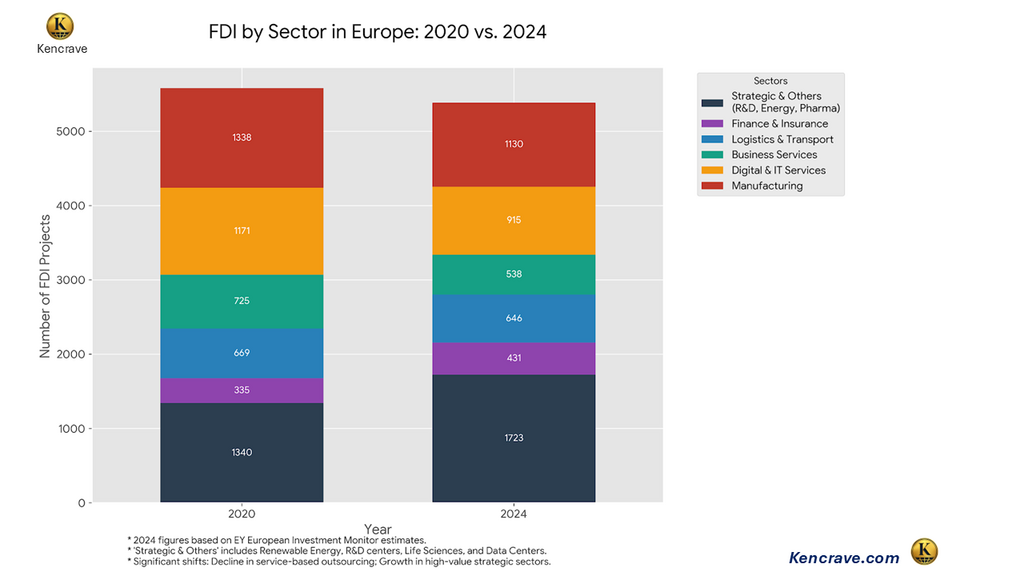

Sectoral Shifts and the Decline of U.S. Investment

A notable feature of recent FDI trends in Europe is the contraction of U.S.-sourced investment. EY reports that jobs created through U.S. investment in Europe have almost halved in recent years, indicating a strategic reorientation toward domestic U.S. production.

FDI by sector in Europe 2020 vs 2024 bar chart showing investment trends across manufacturing, digital services, finance, logistics, and strategic industries.

Europe remains competitive in logistics and segments of the electric vehicle supply chain. However, high-growth sectors like advanced semiconductors, artificial intelligence, and green energy manufacturing, are increasingly gravitating toward North America and East Asia, where incentives are larger and deployment is faster.

What Europe Can Do: Policy Levers to Restore Investment Appeal

To reverse these trends, Europe must move from diagnosis to action. Key reforms could include:

Regulatory simplification: Streamlining permitting, harmonizing standards across member states, and reducing overlapping reporting requirements.

Targeted fiscal incentives: Coordinated EU-level tax credits and subsidies for strategic sectors such as semiconductors, batteries, AI, and clean energy.

Energy cost stabilization: Long-term power pricing mechanisms for industrial users and accelerated grid investment.

Single-market deepening: Faster cross-border project approvals and unified capital markets to support large-scale investments.

These measures would not replicate U.S. or Chinese models but could restore predictability and scale, two qualities investors value most.

Capital reallocation in strategic assets chart showing Europe’s shift 2020 to 2024 with global investment flows to USA, South East Asia, and China driven by industrial policy and geopolitical realignment.

Long-Term Implications for European Competitiveness

Persistently lower FDI threatens Europe’s position in critical future industries. Reduced investment in AI, renewable energy, and advanced manufacturing may:

Slow productivity growth.

Weaken innovation ecosystems.

Limit high-skilled job creation.

Over time, this could widen the economic gap between Europe, the United States, and Asia.

Bottom Line

Nonetheless, the EY Europe Attractiveness Survey notes cautious optimism. If regulatory reform and industrial coordination materialize, Europe can still leverage its strengths: political stability, skilled labor, and a large consumer market. This optimism is partly underpinned by nascent EU initiatives like the Net-Zero Industry Act and ongoing efforts to advance the Capital Markets Union, which aim to directly address some identified barriers.

Key Takeaways: Foreign Direct Investment in Europe

Europe’s FDI decline reflects structural weaknesses, not just a temporary global slowdown.

Geopolitical risk and regulatory complexity have become decisive deterrents for investors.

The U.S. and China are attracting capital through scale, speed, and aggressive industrial policy.

Central and Eastern Europe are disproportionately affected, widening intra-EU divergence.

Recovery depends on regulatory simplification, energy cost stabilization, and coordinated EU-level industrial strategy.

FAQ: Foreign Direct Investment in Europe

1.Why is FDI falling in Europe in 2025? FDI is declining due to geopolitical risk, regulatory complexity, high energy costs, and stronger incentives in the U.S. and China.

2. Which European countries are most affected? Central and Eastern European states have seen the largest drops, with Poland experiencing nearly a 50% decline in inflows.

3. Is Europe losing competitiveness? Relative to the U.S. and China, Europe is struggling to offer the same scale, speed, and certainty for investors in strategic sectors.

4.Can FDI in Europe recover? Yes, but recovery depends on regulatory simplification, coordinated industrial policy, and energy market reform.

The World Economic Forum (WEF) Annual Meeting 2026 in Davos, Switzerland (January 19-23) convened nearly 3,000 leaders under the theme “A Spirit of Dialogue.” The meeting reflected a convergence of...

.png)

.png)

.png)