North American Markets 2026 AI Tech Revival and Q2 investment strategy chart highlighting tech, industrials, energy, financials, defensive, and cash buffer sectors in a digital cityscape. Image Credits: Kenneth Njoroge | Kencrave

North American Markets 2026: Ai Tech Revival, Oil Shock Aftermath, And Q2 Investment Strategy

North American Stock Market Overview (April 2026) North American markets in April 2026 had a turnaround after a turbulent first quarter of the year marked by oil-driven inflation fears and geopolitical uncertainty. The month began with more caution from investors seeking to reduce their exposure to risky assets in favor of more stable investments.

March’s oil shock was a key trigger for this cautious behavior. The month ended with renewed optimism as technology earnings, particularly in AI and semiconductors, reignited market confidence.

Performance of Major North American Stock Indices in April 2026

Nasdaq-100 (U.S.): Surged 15.7%, its strongest monthly gain since 2002, driven by semiconductor and AI infrastructure demand with strong corporate earnings from Nvidia, AMD and Microsoft’s Azure.

S&P 500 (U.S.): Rose 10.5%, reaching fresh highs as broad-based earnings from most of the companies in the S&P 500 exceeded earnings expectations.

Dow Jones Industrial Average (U.S.): Gained 7.2%, supported by industrials and financials. Industrials benefited from infrastructure spending, reshoring trends, and improving manufacturing activity, while financials saw stabilization in equity markets and stronger trading revenues.

Russell 2000 (U.S. small caps): Climbed 12.3%, benefiting from risk-on sentiment and easing oil prices. The rebound was attributed to investors’ rotation into smaller companies after March’s oil shock, and to easing oil prices, which reduced inflationary fears and supported cyclical sectors.

TSX Composite (Canada): Cyclical sectors played a central role in April’s rebound, helping Canadian equities regain momentum as investor sentiment improved. Energy stocks, which had surged earlier in the year, showed a more measured performance in April, slipping about 3.5% among large caps as the sector consolidated despite oil prices remaining elevated.

In contrast, financials and industrials delivered gains, rising 5.6% and 7.9% respectively, providing much of the support behind the TSX’s advance. The materials sector also contributed meaningfully, climbing 8.3% on the back of strong mining and resource-linked companies, underscoring the resilience of Canada’s commodity-driven market.

IPC (Mexico): IPC declined modestly, closing lower by about 0.3% for the month. While industrial exporters and consumer staples provided some resilience, the overall index performance was negative.

What Happened in North American Markets During Q1 2026?

During the first quarter of 2026, North American markets came under pressure from surging oil prices, persistent inflation, and investor unease about the disruptive impact of artificial intelligence. The S&P 500 slipped 4.6%, while the Nasdaq Composite dropped 7.9%, underscoring broad weakness across growth and cyclical sectors.

Technology and communication services bore the brunt of the sell-off in March, when Brent crude spiked above $119 and fears of stagflation weighed heavily on investors’ sentiment.

Defensive areas such as health care, consumer staples, and utilities managed to hold up better, but their resilience was not enough to counterbalance the drag from energy volatility and the rotation away from high-growth sectors.

However, corporate earnings remained stronger than expected, with revenue growth and earnings surprises laying the foundation for the sharp rebound that followed in April.

Key Events and Market Drivers

Oil Price Shock Aftermath: Brent crude spiked above $119 in March due to Middle East conflict, but April saw easing as ceasefire talks progressed. WTI crude stabilized below $100, reducing stagflation fears.

AI & Semiconductor Earnings Super-cycle: Nvidia reported $44.1 billion, up 12% from Q4 and up 69% from 2025, while AMD posted record GPU sales and reported first quarter revenue of $10.3 billion, gross margin 53%, operating income $1.5 billion, net income $1.4 billion and diluted earnings per share $0.84. Microsoft reported a positive overall cloud growth, with AI cited as a major contributor.

Corporate Earnings Season: Corporate earnings broadly exceeded forecasts in banking, industrials and the consumer staples sector. Surprises were especially notable in banks, which benefited from strong trading revenues and capital markets activity. Industrials were supported by infrastructure spending and reshoring trends, and consumer staples showed resilience amid easing inflation.

Policy Uncertainty: Investors remained cautious as central banks balanced inflation control with growth support.

Best Performing Sectors in North American Markets (April 2026)

Technology (AI & Semiconductors): Nvidia, AMD, Microsoft, and Apple led gains, supported by cloud and AI adoption.

Industrials: Caterpillar’s Q1 2026 showed a 22% revenue increase to $17.4B, driven by strong demand in Construction Industries, which grew 38%, supported by U.S. infrastructure projects and manufacturing reshoring.

GE Vernova was a key winner in the industrial space by reporting record Q1 orders, up 71% organically, with a massive $163B backlog, driven by electrification, grid upgrades, and power infrastructure investment.

Financials: JPMorgan Chase benefited from heightened volatility in rates, commodities, and FX markets resulting in gains of its fixed income and equities. Goldman Sachs delivered stronger than expected trading revenue, especially in FICC (Fixed Income, Currencies & Commodities). Volatile markets boosted clients’ demand for hedging, derivatives, and macro trading which are core strengths for Goldman.

Energy (Oil & Gas): ExxonMobil consolidated its strong gains in late 2025 and early 2026 with stable earnings due to crude prices and strong refining margins. Also, Chevron consolidated its earlier gains. Chevron, Valero and other refiners (Marathon Petroleum, Phillips 66) remained highly profitable due to strong refining margins, high diesel and jet fuel demand.

Worst Performing Sectors in April 2026

Airlines: United, Delta, and American Airlines struggled with high jet fuel costs and soft demand despite easing crude prices. Sector ETFs (JETS) were down in April, reflecting this broad weakness in air transport.

Retail: Inflation remained sticky, especially in food and services, squeezing discretionary budgets. Target reported sluggish discretionary sales, especially in apparel and home goods, while Macy’s showed soft foot traffic and continued pressure on mid-income consumer.

Utilities: Duke Energy and ConEd underperformed compared to broad market and its peers as investors rotated into high-growth sectors such as technology, communication services, and industrials, leaving defensive sectors behind. Rising long-term yields also pressured utilities, which are rate sensitive.

Despite underperformance by Duke Energy in April, it reported significant profit for the first quarter of the year 2026 with a net income of $1.55 billion, an increase from $1.38 billion in the first quarter of 2025 with Data centre as a ley driver.

Key Company Highlights for April 2026

Outperformers: Nvidia, AMD, Microsoft, Apple, ExxonMobil and Chevron

Underperformers: United Airlines, Delta Airlines, Target, Macy’s and Duke Energy

How North American Central Banks Responded in Q12026

The Federal Reserve (U.S.)

The Federal Reserve through the Federal Open Market Committee (FOMC) held the federal funds rate at around 3.50%-3.75%. The decision to have the rate unchanged was driven by higher-than-expected inflation readings, geopolitical uncertainty (Iran conflict) and mixed labor market signals. The Fed expects gross domestic product to grow to 2.4% this year with the unemployment rate projected to remain at 4.4% by year end.

Bank of Canada

The Bank of Canada maintained the policy rate at 2.25% influenced by a cooling economy, geopolitical uncertainties due to the Middle East conflict and navigating U.S. trade (tariffs) policies. Despite a rise in inflation due to higher oil prices linked to the Middle East conflict, the bank anticipates inflation will ease back to the 2% target in 2027. Growth in potential output for Canada is expected to average 1.2% in 2026 before picking up modestly to 1.3% in 2027 and 1.5% in 2028.

Banxico (Mexico)

Mexico’s monetary policy path in early 2026 reflected Banxico’s gradual easing stance as the central bank balanced persistent inflation pressures with weakening economic activity. Following its March 26 decision to lower the benchmark rate to 6.75%, Banxico kept the policy rate unchanged throughout April 2026.

It maintained a cautious posture as inflation remained elevated due to higher energy prices and geopolitical tensions. After reviewing April inflation data and broader economic conditions, the Governing Board moved again in early May, reducing the rate to 6.50% to support a slowing economy while still signaling vigilance toward inflation risks.

Key Risks Ahead

Risks to Watch Heading Into the second quarter of 2026:

1. Energy and Geopolitical Volatility

Despite April’s easing in oil prices, the Middle East conflict remains the most significant macro risk heading into Q2 2026. Any renewed escalation could quickly reverse recent progress, pushing Brent crude back toward the $110–$120 range and reviving fears of stagflation.

Such a move would pressure transportation, consumer discretionary, and industrial sectors while forcing central banks to remain cautious. Markets are still highly sensitive to energy-driven inflation, making geopolitical developments a critical risk to monitor.

2. Inflation Persistence and Central Bank Divergence

Inflation has moderated from the March spike but remains sticky in services, food, and energy. If price pressures fail to ease further, the Federal Reserve and Bank of Canada may delay any shift toward policy easing, while Banxico, which is already cutting rates, may be forced to slow its pace.

This growing difference in monetary policy across North America raises the risk of FX volatility, tighter financial conditions, and uneven capital flows. A higher‑for‑longer rate environment would weigh heavily on rate‑sensitive sectors such as utilities, real estate, and small‑cap companies.

3. Sustainability of the Tech‑Led Rally

April’s powerful rebound was driven by exceptional earnings from AI and semiconductor leaders, but expectations are now somewhat elevated. Any signs of slowing AI infrastructure spending, semiconductor supply constraints, or margin pressure could trigger a sharp rotation out of the big technology stocks.

Given that tech leadership accounted for much of April’s market strength, the durability of this earnings momentum is a key risk for Q2. A disappointment in the next earnings cycle could undermine broader market sentiment.

4. Consumer and Credit Fragility

While markets rallied in April, underlying consumer and credit conditions remain fragile. Mid‑ and low‑income households continue to face pressure from elevated service and food inflation, weighing on discretionary retail and travel.

At the same time, higher borrowing costs among small businesses pose risks to financial stability. If labor market momentum softens or inflation remains persistent, consumer‑facing sectors and credit‑sensitive industries could experience renewed stress in the second quarter.

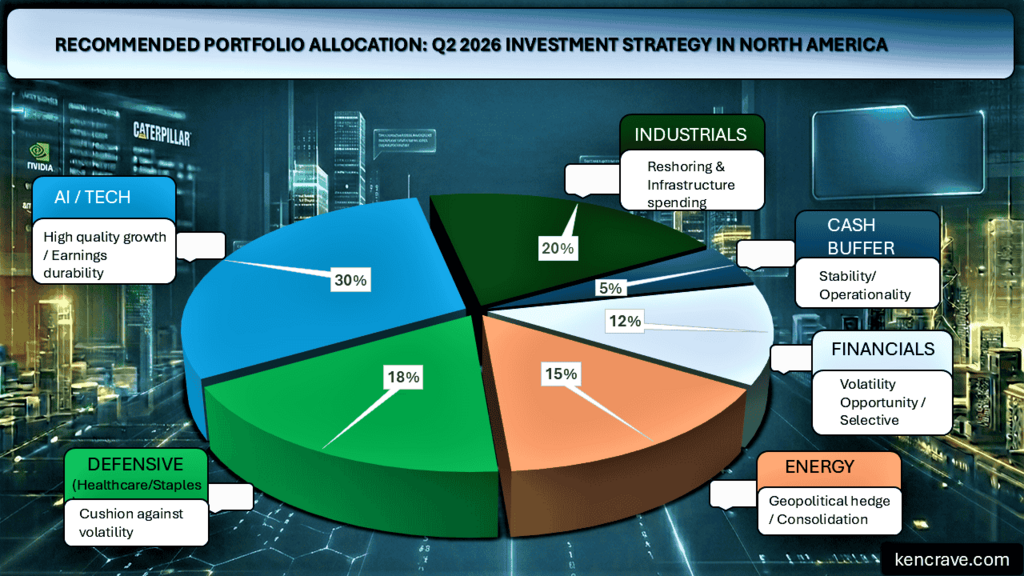

Recommendations Investment Strategies for Q2 2026

North American markets enter the second quarter with renewed momentum following April’s strong rebound, but the environment remains highly sensitive to energy prices, inflation dynamics, and central bank policy divergence.

Against this, investors may consider a balanced, risk‑aware approach that emphasizes cash stability, resilience, and selective exposure to growth themes.

Q2 2026 North America investment strategy pie chart showing AI Tech 30%, Industrials 20%, Defensive 18%, Energy 15%, Financials 12% and Cash Buffer 5%.

1. Maintain Exposure to High‑Quality Growth, but Prioritize Earnings Durability

The April rally was driven by exceptional results in AI, semiconductors, and cloud infrastructure. These areas remain structurally supported by long‑term demand, but expectations are now elevated. Investors may benefit from focusing on companies with strong balance sheets, clarity on AI‑related revenue streams, proven pricing power, and supply chain resilience.

2. Balance Portfolios with Cyclical and Defensive Assets

With inflation still sticky and geopolitical risks unresolved, diversification across cyclical and defensive sectors remains important. Industrials, energy infrastructure, and materials continue to benefit from reshoring, grid modernization, and infrastructure spending.

Having defensive sectors such as healthcare and consumer staples could cushion the portfolio if consumer spending weakens or if markets react to renewed oil price volatility.

3. Monitor Rate‑Sensitive Areas as Central Bank Paths Diverge

The Federal Reserve and Bank of Canada are holding rates steady, while Banxico has begun easing as of early May 2026. This divergence increases FX volatility and affects rate‑sensitive sectors. Consider being cautious with utilities, REITs, and highly leveraged companies.

Watch for opportunities in financials benefiting from trading activity and stable credit conditions. Consider the impact of currency swings on cross‑border earnings.

4. Stay Selective in Consumer‑Facing Sectors

Consumer conditions remain uneven, with mid‑income households still pressured by elevated service and food inflation. Investors could consider focusing on companies with strong brand loyalty, pricing power, exposure to essential goods or services, and lower sensitivity to discretionary spending cycles.

Investor Outlook Q2 2026

Looking ahead, Q2 2026 is likely to favor technology and selective energy exposure, but investors must remain vigilant against geopolitical shocks and inflationary pressures. A balanced, sector‑focused strategy will be critical to navigating the evolving North American market landscape.

Recommendations for Governments and Key Stakeholders (Q2 2026 Outlook)

1. Prepare for Oil Shocks

Governments should set clear rules for when to release emergency oil reserves, allow temporary flexibility for refineries and transport logistics, and offer short‑term help to households most affected by fuel costs without using expensive subsidies.

2. Manage Policy Differences Across Countries

The U.S. and Canada should check how businesses would handle interest rates staying high for longer. Mexico should pair its rate cuts with clear communication and strong fiscal planning to avoid sudden capital outflows.

3. Support Tech Growth Without Creating Dependency

Governments should encourage AI and semiconductor investment through stable, long‑term tax policies rather than short‑term subsidies. Any public investment in power grids or electrification should still make sense even if AI spending slows.

4. Address Consumer and Credit Weakness Early

Regulators should move from simply watching risks to actively stress testing small banks and loans in vulnerable sectors like retail and travel. They should design quick‑to‑activate support tools, such as temporary tax credits, in case job markets weaken.

Key Takeaways

Investor sentiment shifted rapidly from defensive positioning to aggressive risk-taking during April 2026.

Market leadership broadened beyond high-cap tech, with industrials, materials, and small caps also participating in the rebound.

Policy divergence across the U.S., Canada, and Mexico is becoming an increasingly important driver of capital flows and currency volatility.

Earnings resilience proved more important to market than just macroeconomic uncertainty and geopolitical risks.

Q2 2026 may reward selective positioning rather than broad market exposure as volatility and sector dispersion remain elevated.

Frequently Asked Questions About North American Markets in 2026

1. Why did AI stocks surge in April 2026? AI stocks surged because of strong semiconductor earnings, growing cloud demand, and accelerating investment in AI infrastructure.

2. How did oil prices affect stock markets in 2026? Higher oil prices increased inflation fears and pressured transportation and consumer sectors, while benefiting energy companies.

3. Which sectors may outperform in Q2 2026?

Technology, industrials, AI infrastructure, energy infrastructure, and selective financials may continue outperforming.

4. What are the biggest risks for investors in Q2 2026? Key risks include oil price volatility, persistent inflation, central bank policy uncertainty, and slowing consumer demand.

5. Will the Federal Reserve cut interest rates in 2026? Markets remain uncertain as inflation has moderated but remains above target levels. Future policy decisions will depend on inflation and labor market data.

North American markets closed sharply lower on March 20, 2026, capping a volatile week marked by surging oil prices and escalating geopolitical tensions in the Middle East. The S&P 500,...