From M-Pesa to fintech regulation, Kenya’s step-by-step approach to digital finance offers lessons for policymakers, investors, and emerging markets worldwide.

Kenya’s digital finance ecosystem is widely regarded as the most advanced in emerging markets, driven by mobile money, fintech innovation, and adaptive regulation. This analysis explains how Kenya built its digital finance model, why it succeeded, and what risks and opportunities lie ahead.

Kenya did not become a global leader in digital finance through disruption alone. Instead, it followed a deliberate, layered strategy that combined mobile money innovation, adaptive regulation, and widespread mobile access. Today, more than 85% of Kenyan adults use formal financial services, a transformation driven by choices made over two decades.

Mobile money adoption and branchless banking have significantly increased financial inclusion, with access to formal financial services rising from 27 % in 2006 to 85 % in 2024 (Central Bank of Kenya, 2025). Investments in digital infrastructure have further strengthened the reliability and scalability of financial services, establishing Kenya as a benchmark for digital finance in emerging markets (GSMA, 2024).

Kenya’s financial sector has developed through a layered process. Each stage of reform leveraged existing institutional, regulatory, and technological foundations, reinforcing system resilience and enabling incremental innovation. Mobile money platforms and branchless banking models demonstrate how regulatory guidance, infrastructure development, and market demand intersect to expand financial access and foster sustainable digital finance growth.

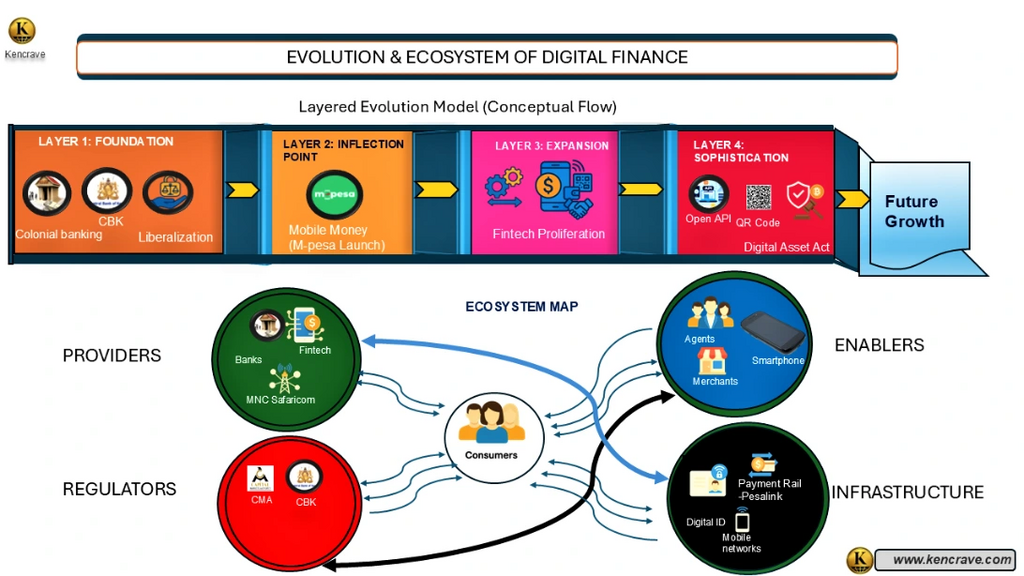

This transformation can be explained using a dual framework that shows both its historical path and its current complexity. Kenya’s digital finance sector has grown in clear stages, with each layer building upon the one before it. This step-by-step growth created today’s interconnected ecosystem, where providers, enablers, regulators, and infrastructure work together around the consumer and MSMEs.

Kenya digital finance evolution ecosystem map showing colonial banking, M-Pesa, fintech, open API, QR codes, digital assets, regulators, providers, enablers, and infrastructure

The framework highlights this dual view. The Layered Evolution Model shows the progression from early banking reforms to mobile money, fintech growth, and today’s interoperable systems. The Ecosystem Map shows the resulting market structure, centered on the Consumer and MSMEs, supported by the interdependent roles of Providers, Enablers, Regulators, and Infrastructure.

Foundations of Kenya’s Financial System

Early Banking in Kenya: Colonial Origins and Post-Independence Financial Reforms

Kenya’s formal banking system originated during the colonial period, when financial services were designed to support trade finance, settler agriculture, and government administration. Before independence, currency and monetary functions were handled by the East African Currency Board, and formal banking services were concentrated among foreign banks, with limited access for the majority of Kenyans.

After independence in 1963, the government prioritized financial sovereignty by establishing the Central Bank of Kenya in 1966, taking over currency issuance and regulatory functions, and supporting the creation of locally owned institutions such as the Co‑operative Bank of Kenya to extend services beyond elite urban clients.

Summary: The Hidden Precondition Kenya’s digital finance success rests on decades of institutional groundwork. Without a central bank, liberalized markets, and competitive retail banking, mobile money would not have scaled safely or sustainable.

Financial Liberalization in Kenya: Market Expansion and Private Sector Growth

Major financial sector reforms in the 1980s and 1990s liberalized interest rates, reduced state controls, and encouraged private sector participation. These reforms improved competition, expanded product diversity, and enabled new banking models to emerge, which in turn supported greater outreach to previously underserved populations.

Retail‑focused banks like Equity Bank took advantage of the more open environment by targeting low‑income customers and small businesses that had limited access to formal banking services outside urban centers.

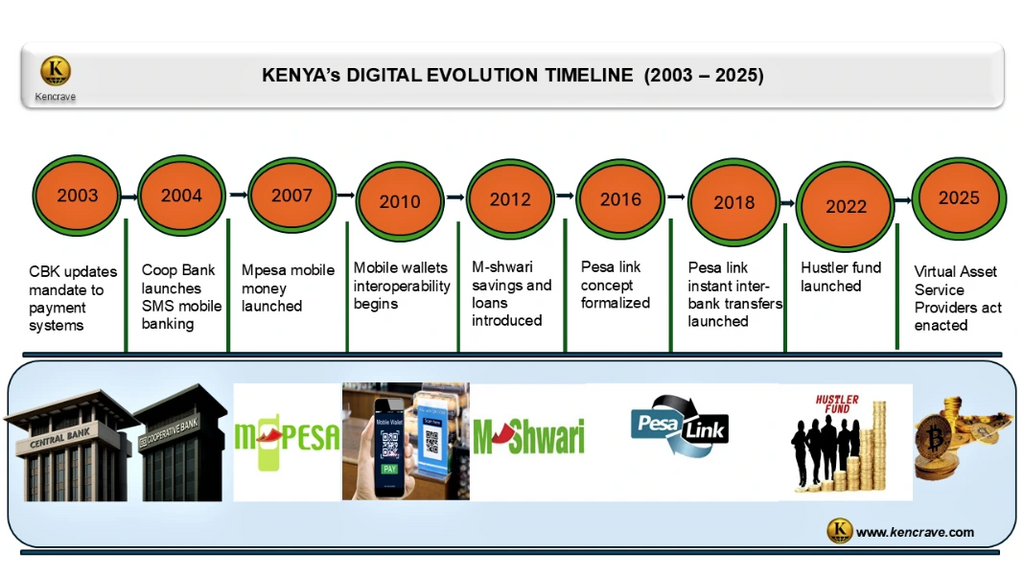

Timeline of Kenya’s Digital Financial Evolution Key Milestones in Kenya’s Digital Finance and Mobile Money Growth

Kenya digital finance timeline 2003–2025 highlighting CBK reforms, M-Pesa launch, mobile wallets, M-Shwari, PesaLink, Hustler Fund, and Virtual Asset Service Providers Act.

TheMobile Money Inflection Point

1. M-Pesa in Kenya: How Mobile Money Transformed Financial Access

The launch of M‑Pesa by Safaricom in March 2007 marked a significant inflection point in Kenya’s financial system. M‑Pesa provided a way for users to store and transfer money using mobile phones and a nationwide agent network, eliminating the need for traditional bank accounts and physical branches for many everyday transactions. This service was designed as an electronic payment and store of value system accessible on ordinary mobile devices and quickly expanded its user base due to the simplicity and reach of the mobile platform.

Kenya’s financial regulators adopted a cautious but facilitative approach that allowed mobile money to scale while monitoring risks to consumers and systemic stability. This balance of oversight and flexibility is widely cited as a key factor in enabling the mobile money sector to grow without unduly constraining innovation or financial inclusion.

Summary: Why M-Pesa Worked M-Pesa succeeded not just because of technology, but because regulators allowed it to grow outside rigid banking rules while maintaining oversight. This balance unlocked rapid adoption without eroding trust. 2. Mobile Money Adoption in Kenya and Its Impact on Financial Inclusion

Mobile money adoption expanded rapidly across Kenya in the years after M‑Pesa’s launch. Data from the 2024 FinAccess Household Survey shows that formal financial inclusion rose from approximately 27% of adults in 2006 to 80% by the early 2020s, with mobile money accounts accounting for the majority of this increase. By 2024, formal financial access reached around 85% of adults, reflecting near‑universal access to some form of formal financial service, driven largely by widespread mobile money use.

These changes show how a combination of technological adoption, regulatory support, and demand for accessible financial tools can reshape a country’s financial landscape. Mobile money has become a central component of Kenya’s digital finance market and a major driver of expanded financial inclusion.

Summary: Access vs Depth Kenya solved financial access faster than almost any country. The remaining challenge is financial depth: savings, insurance, pensions, and long-term credit still lag behind transactional use.

Bar Chart showing: Kenya’s Mobile Money Transaction Intensity (2007–2024)

Data source: Central Bank of Kenya.

Kenya Mobile Money Transactions (2007–2024): Key Observations and Insights

Mobile money transaction volumes in Kenya have surged from KSh 16.3 billion in 2007 to KSh 8,697.7 billion in 2024.

2007–2009: Transactions jumped from KSh 16.3 billion to KSh 473.4 billion, reflecting rapid early adoption after launch.

2010–2015: Growth was steady, with annual increases of KSh 300–400 billion, showing market consolidation and rising trust in mobile money.

2016–2020: Growth picked up again, surpassing KSh 5 trillion by 2020, driven by new services like merchant payments and government disbursements.

2021–2024: Growth slowed, with 2023 showing a near plateau at KSh 7,953.9 billion compared to KSh 7,908.8 billion in 2022, suggesting possible market saturation.

Summary: Signs of Saturation Mobile money growth has slowed as user adoption nears saturation. Future expansion will come from merchant payments, SME services, and integrated financial products not new users. Mobile money is now a core financial service in Kenya.

Digital Banking and Fintech Development

1. Digital Banking in Kenya: How Banks Adapted to Mobile and Online Finance

As mobile money and digital financial services expanded in Kenya, traditional banks accelerated their digitization efforts. Mobile banking applications, USSD services, and wallet integrations became standard offerings as banks responded to changing customer preferences and widespread mobile connectivity. Rising smartphone adoption and lower data costs have supported this shift, increasing mobile banking usage across urban and rural populations.

Despite these digital changes, banks remain central to deposit mobilization, large-scale credit provision, and regulatory compliance. The move toward digital channels has improved operational efficiency and customer access, but banks continue to serve as core financial intermediaries within the broader financial system.

Summary: Banks Were Not Displaced Fintech and mobile money changed delivery channels, not financial fundamentals. Banks remain central to deposits, credit, and compliance, while fintech firms expand reach and efficiency.

2. Fintech Growth in Kenya: Digital Lending, Payments, and Insurtech

Kenya hosts one of Africa’s most developed fintech ecosystems, featuring a large and diverse set of firms operating across various financial technology segments, including payments, digital lending, and insurtech. The number of fintech startups in Kenya has grown rapidly, with hundreds of firms active across multiple sub‑sectors, reflecting the country’s supportive environment for fintech innovation (Business Daily Africa, 2025).

Digital lenders, such as Tala and Branch, expanded access to short-term credit by utilizing alternative data sources and mobile platforms, thereby improving credit access for many users beyond traditional bank customers (Kenya Bankers Association, 2023).

While this expansion increased financial access, it also raised concerns about consumer over‑indebtedness and data protection, prompting regulators to strengthen licensing and consumer protection requirements for digital lenders. Insurtech and digital investment platforms remain emerging areas with growth potential due to relatively low market penetration compared to payments and lending.

Summary: Where Innovation Is Concentrated Kenya’s fintech ecosystem is strongest in payments and digital lending. Insurtech, wealth tech, and long-term savings remain underdeveloped, representing the next growth frontier.

The Current Market Structure of Kenya’s Digital Finance Market

FinAccess survey data shows a clear hierarchy in financial product use among Kenyan adults. Mobile money services are used by more than 80 percent of adults, while bank account ownership is lower but trending upward. Insurance, pension, long-term savings, and investment products have much lower usage rates compared to mobile money and banking services.

This indicates that most users engage with basic transactional tools rather than deeper financial products. These patterns suggest that while Kenya has largely solved financial access, the depth of financial engagement remains limited (Central Bank of Kenya, 2024).

2. Financial Product Usage in Kenya: Mobile Money, Banking, and Financial Depth

Mobile money systems process large transaction volumes, reflecting their central role in Kenya’s financial landscape. Central Bank of Kenya payment systems data show that mobile money monthly transaction values reached hundreds of billions of Kenyan shillings, and the total count of active subscriptions and agents continues to expand.

This scale reflects the broad use of mobile money but should not be conflated with market revenue or direct economic contribution. Independent market research projects Kenya’s digital payments market to grow into the low to mid-teens in billions of US dollars by the late 2020s, driven by e-commerce, merchant payments, and wallet usage (Central Bank of Kenya, 2025).

3. Digital Finance Regulation in Kenya: Payments, Digital Credit, and Consumer Protection

Kenya’s regulatory framework has changed with innovation in financial services. The Central Bank of Kenya’s National Payments System regulations require mobile money platforms to support interoperability and govern payment service providers. TheCentral Bank of Kenya (Digital Credit Providers) Regulations, 2022require digital lenders to be licensed and follow consumer protection and data privacy rules under the Data Protection Act, 2019.

Regulatory sandboxes allow firms to test new products in a controlled environment before full launch. TheCapital Markets Authority’s Regulatory Sandbox Policy Guidance Note 2019 lets fintech firms trial innovations under oversight, helping regulators balance innovation with market stability.

Summary: Regulation as an Enabler Kenya’s regulators consistently prioritized flexibility over restriction. Sandboxes, interoperability rules, and digital credit licensing allowed innovation while gradually strengthening consumer protection.

4. Cryptocurrency Adoption in Kenya and the Regulatory Response

Chainalysis data from the 2023 Global Crypto Adoption Index show that Kenya is one of the leading countries in peer-to-peer cryptocurrency usage, with high P2P exchange trade volume driven in part by remittances and informal trading outside the formal financial system.

Kenya’s Digital Asset Policy and the Virtual Asset Service Providers Act

The Kenyan government has began formal policy work on digital assets, including the passage of the 2025 Virtual Asset Service Providers Act, to regulate virtual asset service providers and address consumer protection and anti-money-laundering concerns. Kenya has not issued a central bank digital currency as of 2025, and recent policy updates note that the case for a CBDC is not compelling at this time.

Summary: High Usage, Cautious Policy Kenya ranks high in peer-to-peer crypto usage, but policymakers remain cautious. Regulation is evolving to manage risk without endorsing digital assets as core financial infrastructure.

Future of Digital Finance in Kenya: Growth Opportunities and Systemic Risks

Kenya’s digital finance sector is expected to grow through stronger payment systems, expansion of SME digital lending, growth in insurtech, and deeper integration of financial platforms. At the same time, the sector faces risks from household over-indebtedness, rising cybercrime threats, regulatory lag, and uneven levels of digital literacy among users (Research and Markets report, 2025).

Summary: What Comes Next Kenya’s next phase of digital finance growth depends less on technology and more on trust: cybersecurity, digital literacy, responsible credit, and institutional capacity will determine outcomes.

Blockchain and Digital Assets in Kenya: Disruption or Complement to Mobile Money?

Blockchain and digital assets could disrupt platforms like M-Pesa by enabling low-cost, cross-border, peer-to-peer transactions without intermediaries, which may reduce transaction fee revenues. At the same time, these technologies can help manage existing risks through smart contracts that improve loan transparency and reduce fraud, and through blockchain-ledgers that support real-time regulatory oversight. Kenya’s challenge will be to adopt these innovations within strong regulatory frameworks to promote financial inclusion while avoiding systemic risks.

According to the World Data Bank, the digital finance market will expand steadily rather than explode. Growth will depend on institutional trust, clearer regulation, and broader digital skills and infrastructure. World Bank initiatives like the Kenya Digital Economy Acceleration Project stress that closing gaps in digital literacy and strengthening trust are essential for sustained growth.

Summary: Threat or Tool? Blockchain could pressure mobile money fees over time, especially in cross-border payments. Its impact will depend on usability, regulation, and whether it complements existing systems rather than bypassing them.

Who Powers Kenya’s Digital Finance Ecosystem? Regulators, Banks, Fintechs, and MNOs

Regulators and policymakers: The Central Bank of Kenya oversees banks, mobile money operators, payment service providers, and digital credit providers. The Capital Markets Authority regulates digital investment platforms and runs the regulatory sandbox. The Office of the Data Protection Commissioner enforces data privacy rules.

Mobile network operators: Safaricom leads through M-Pesa. Airtel Kenya and Telkom Kenya support competing mobile money platforms. These firms provide the infrastructure, agent networks, and distribution that anchor digital finance adoption.

Commercial banks: Banks such as Equity Bank, KCB, Co-operative Bank, and Absa Kenya provide deposits, credit, treasury services, and compliance functions. They integrate mobile and digital channels with core banking services.

Fintech companies: Payment firms, digital lenders like Tala and Branch, insurtech startups, and wealth tech platforms drive product innovation. They expand access to payments, short-term credit, and emerging digital financial products.

Agents and merchants: Mobile money agents, retail merchants, and SMEs enable cash-in and cash-out services, merchant payments, and last-mile access across urban and rural areas.

Consumers and businesses: Households, microenterprises, SMEs, and corporates use mobile money, banking, and fintech services for payments, savings, credit, and business operations.

Development partners and investors: Institutions such as the World Bank, GSMA, and private investors fund infrastructure, research, pilots, and scale-up of digital finance solutions.

Summary: Coordination Is the Advantage Kenya’s digital finance strength lies in coordination. Regulators, banks, mobile operators, fintech firms, agents, and consumers all play defined roles within a shared framework.

Policy Recommendations for Kenya’s Digital Finance Sector (Short-Term Priorities)

Policymakers should strengthen enforcement of existing digital credit and data protection regulations. Over-indebtedness and misuse of customer data remain active risks. Better supervision improves trust and reduces systemic fragility.

Regulators should expand and speed up regulatory sandbox approvals for insurtech, SME finance, and wealth platforms. Payments are mature, but these segments remain underdeveloped.

Investors should focus on fintech firms that improve efficiency within the existing ecosystem. Examples include merchant payment tools, SME cash flow management, and compliance technology. These address real gaps without betting on untested consumer behavior.

Summary: Short Term Action The immediate priority is trust: enforcing digital credit rules, protecting consumer data, and improving supervision of fast-growing fintech segments.

Medium-Term Strategies for Fintech Growth and Financial Deepening in Kenya

Policymakers should promote deeper financial usage, not just access. Incentives for long term savings, pensions, and micro insurance can shift users from transactional wallets to wealth-building products.

Interoperability should be enforced across banks, mobile money platforms, and fintech wallets to reduce market fragmentation and lower transaction costs.

Investors should target scalable platforms that embed finance into non-financial services such as agriculture, logistics, health, and e-commerce. Embedded finance improves adoption and unit economics.

Summary: Medium Term Action Growth will come from financial deepening: pensions, insurance, SME finance, and embedded financial services not from basic payments.

Long-Term Policy and Investment Priorities for Kenya’s Digital Finance Infrastructure

Policymakers should invest in national digital skills and cybersecurity capacity. Digital finance growth now depends more on trust and resilience than on access.

Clear, adaptive frameworks for digital assets and cross-border payments are needed to prevent regulatory arbitrage while supporting innovation.

Investors should prioritize infrastructure-level opportunities such as payment rails, regtech, credit bureaus, and identity systems. These offer lower volatility and long-term returns as the ecosystem matures.

Summary: Long Term Action Long-term resilience depends on infrastructure investments: digital skills, cybersecurity, identity systems, and adaptive regulation for cross-border finance and digital assets.

Key Takeaways

Kenya’s digital finance success followed a deliberate, step-by-step path built on early banking and regulatory reforms. These foundations enabled mobile money and later fintech growth.

M-Pesa marked the major turning point from bank-led to user-centered finance. It drove financial inclusion from 27% in 2006 to over 85% by 2024.

Regulation balanced innovation and stability. Policies from 2003 to 2025 created trust, managed risk, and supported sector growth.

The ecosystem relies on collaboration between providers, enablers, regulators, and infrastructure.

Access to digital finance is widespread, but advanced services remain underused. Future growth depends on expanding savings, insurance, and responsible credit use.

Innovation has moved beyond payments to savings, lending, interoperable transfers, and digital assets. SME finance and embedded services will drive the next phase.

Growth prospects are strong but face risks like cybercrime and over-indebtedness. Progress depends on better skills, trust, and inclusive policies.

Summary: Core Lesson Kenya’s experience shows that inclusive digital finance is built through sequencing, regulation, and institutional trust not disruption alone.

Frequently Asked Questions: Kenya’s digital finance model

1. What makes Kenya’s digital finance model different from other countries?

Kenya combined mobile network reach, agent-based distribution, and flexible regulation early. Mobile money scaled before smartphones or widespread banking access, which shaped user behavior and market structure.

2. Is mobile money growth slowing in Kenya?

Transaction value growth has slowed since 2022, suggesting saturation in basic payments. Growth is shifting toward merchant payments, SME services, and integrated financial products rather than new users.

3. Have banks been displaced by mobile money and fintech?

No. Banks remain central to deposits, large-scale lending, and regulation. Mobile money and fintech changed delivery channels and customer interfaces, not the core role of banks.

4. What are the main risks in Kenya’s digital finance sector?

Household over-indebtedness, cybercrime, data misuse, and uneven digital literacy are the key risks. Regulatory capacity and consumer education are now as important as innovation.

5. Are cryptocurrencies a threat to mobile money platforms?

In the short term, no. In the long term, blockchain-based payments could pressure fees on cross-border and peer-to-peer transfers. The impact depends on regulation, usability, and trust.

6. What is the next growth frontier for Kenya’s digital finance ecosystem?

SME finance, insurtech, long-term savings, and embedded financial services. These areas deepen economic impact beyond payments.

7. Can other countries replicate the Kenya model?

Elements can be adapted, but direct replication is unlikely. Kenya’s success depended on timing, regulatory choices, and market structure that are hard to reproduce exactly.

The Economic Cost of Discrimination Against Women-Led Startups

UN Women emphasizes that investing in women is one of the most powerful drivers of economic growth, with the potential to unlock...

IShowSpeed's African Tour and the New Era of Influencer Diplomacy

Darren Jason Watkins Jr., better known as “IShowSpeed”, is an American YouTuber and livestreaming sensation. His high-energy, unpredictable content blends...

What Is Driving Africa’s 2026 Risk Outlook?

Executive Summary

Africa’s 2026 growth and risk landscape is being reshaped by high-stakes agreements and regional macro developments. The Washington Accords between the...

China’s engagement in Africa has expanded dramatically over the past two decades, reshaping economies, trade patterns, and political alliances. As China becomes Africa’s largest trading partner, biggest bilateral lender, and...