Asia’s Space Revolution 2025–2040: How China, India & Japan Are...

Asia Innovation

Move over Houston and Moscow, Asia’s space race is rapidly accelerating, ushering in a new chapter in the global contest for space leadership. Driven by a potent mix of technological ambition, geopolitical strategy, and economic incentives, China, India, and Japan are investing heavily in their space programs. This surge marks a pivotal phase in the global quest to explore and utilize space, with significant long-term implications.

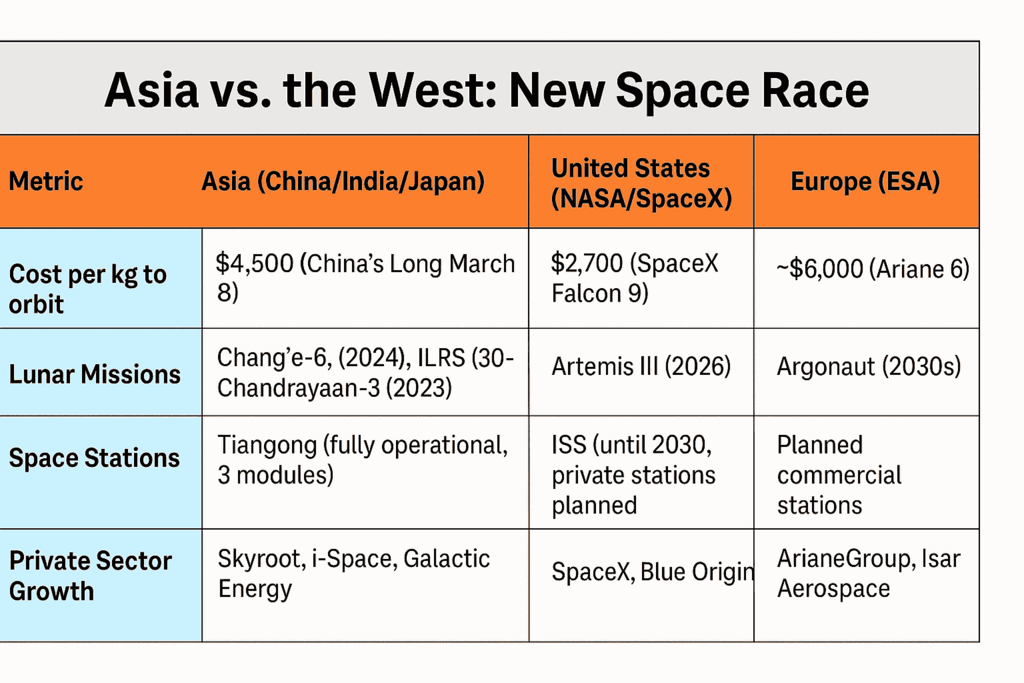

Asia vs. the West: Who Leads the New Space Race?

A comparative overview of key space capabilities reveals the growing competitiveness of Asia’s spacefaring nations.

A Comparative visual of Asia vs Asia Space Exploration in Key metrics

"While Asia is narrowing the gap in launch cadence and mission diversity, the United States still leads in reusability and deep-space exploration." Dr. Radhika Iyengar, Space Policy Fellow, Institute of Strategic Studies

"India and Japan are playing pivotal roles in setting norms and collaborative frameworks, an often-understated dimension of space leadership." Kenji Tsubaki, Senior Analyst, Asia-Pacific Space Security Forum

China, India, Japan: The New Space Titans China

China continues to assertively expand its space program. The Tiangong space station, now fully operational, marks a significant milestone in long-duration human spaceflight. China is also advancing plans for a crewed lunar base by the 2030s in collaboration with Russia under the International Lunar Research Station (ILRS) initiative.

"China’s trajectory in space mirrors its terrestrial strategy—long-term investments with strong state backing," says Liu Zhen, Aerospace Analyst at the Beijing Institute for Space Policy.

India

India maintains a pragmatic yet ambitious posture. Its Chandrayaan-3 mission achieved the world’s first successful landing near the lunar south pole in 2023. India is simultaneously developing its Gaganyaan human spaceflightprogram and participating in NASA's Artemis Accords.

Japan

Japan offers a distinctive contribution focused on governance, robotics, and security. Its SLIM mission demonstrates precision lunar landing technology, while the H3 rocket is being refined to ensure greater cost-efficiency. Japan also plays a central role in debris mitigation through projects like ADRAS-J, aimed at removing orbital debris.

Comparative Timeline Visual of Key Mission Milestones in Space Race (2023–2040)

Technological Breakthroughs & Practical Impact

Across the region, a series of space technology achievements underscore growing capabilities:

China: Tiangong enables extended human presence in orbit; launch infrastructure supports high mission frequency.

India: Chandrayaan-3 success on a limited budget enhances its reputation for cost-effective innovation.

Japan: SLIM and the H3 rocket reflect advances in precision landing and cost-efficient access to space.

Technologies such as reusable launch vehicles, AI-based spacecraft operations, and next-gen satellite constellationsare already delivering real-world benefits:

High-speed internet access in rural India and Indonesia.

AI-powered disaster prediction for regions like the Mekong Delta.

Reduced cost to orbit through partial reuse of launch components.

The Orbital Economy: Asia’s $1 Trillion Opportunity, Market Trends and Projections

Asia’s space economy is expanding rapidly. Government space agencies now coexist with a growing cadre of startups and commercial ventures:

Key Trends & Metrics:

India’s NSIL reported ₹2,940 crore (~$350 million) in revenue for 2022–23, operating 15 communication satellites and overseeing over 120 international satellite launches, New Space India Limited (NSIL) 2023 Report.

China boasts over 430 commercial space firms, with its space economy forecast to reach $900 billion by 2029, (China Briefing).

The Asia-Pacific small satellite market is projected to reach$17.8 billion by end of 2025 and USD 34.11 billion by 2030, growing at a CAGR of 13.89% during this period, Space & Satellite Professional International (SSPI).

Japan’s space industry was valued at $8.6 billion in 2024, with rising private and public investment.

Space tourism in Asia, while nascent, is growing at 20% CAGR and may evolve into a multibillion-dollar segment by the 2030s.

"Asia’s space economy is transitioning from government dominance to a hybrid model where public-private synergy drives innovation," notes Shreya Mehta, Investment Strategist at Orbit Ventures, Singapore.

Challenges: Can Asia Sustain Its Momentum?

Despite notable progress, key challenges could limit Asia’s trajectory:

Geopolitical Tensions: U.S.–China competition may restrict access to critical technologies and collaborative frameworks.

Orbital Debris: Asia contributes approximately 40% of new orbital debris; mitigation efforts like Japan’s ADRAS-J are essential but nascent.

Budget Limitations: India’s space budget remains about 7% of NASA’s, limiting mission scope and frequency.

Lack of Unified Policy: Unlike the European Space Agency or U.S. FAA, Asia lacks a regional regulatory body or policy framework.

Strategic Roadmap: How Asia Can Lead the Next Space Era

Governments

Establish comprehensive, transparent regulatory frameworks to promote investment and innovation.

Invest in education and STEM workforce development tailored to space industry needs.

Encourage regional cooperation via data-sharing, mission coordination, and standards harmonization.

Private Sector

Develop dual-use technologies that serve both civil and defense applications.

Collaborate across national boundaries on shared challenges like debris mitigation and rural connectivity.

Focus on commercially viable downstream services such as precision agriculture, logistics tracking, and environmental monitoring.

Investors

Target high-growth sectors such as reusable launch systems, Earth observation, and in-orbit servicing.

Leverage public co-investment schemes to mitigate risk and catalyze innovation.

Monitor regulatory shifts that may impact long-term ROI and cross-border expansion.

Can Asia Redefine the Future of Space Exploration?

Asia is reshaping the global space race with a pragmatic, technologically advanced, and economically grounded approach. From China’s lunar ambitions to India’s cost-effective missions and Japan’s governance leadership, the region is carving out a multifaceted role in space.

If current trends hold, and challenges are proactively addressed, Asia could not only match but lead in several strategic space domains, redefining how humanity explores, exploits, and governs the final frontier.

Canada’s $1.4 B Talent Crisis: Why 72% Of Stem Graduates...

NorthAmerica Business

Canada has long stood as a beacon of educational excellence, with institutions like the University of Toronto and McGill University consistently ranking among the top 50 globally. Yet, behind this academic prestige lies a sobering reality: Canada has become the world’s most generous talent incubator, for other countries. Despite its investment in human capital, Canada struggles to retain its brightest minds, a challenge deeply tied to gaps in STEM policy and its innovation ecosystem.

Real-World Impact: A Top Grad Heads South

When Maya Cheng graduated from the University of Toronto with a master’s in artificial intelligence, she had job offers from both Toronto and San Francisco. The Toronto offer paid CAD $105,000. The San Francisco startup, flush with venture capital, offered her CAD $210,000 (adjusted for cost of living). “It wasn’t even a hard decision,” she says. Like many of her peers, Maya packed her bags and headed south.

Her story reflects a troubling national trend that threatens Canada’s ability to compete in high-growth sectors like AI, quantum computing, and biotech.

Quantifying Canada’s Brain Drain Problem

Recent data illustrates how severe the tech sector migration has become:

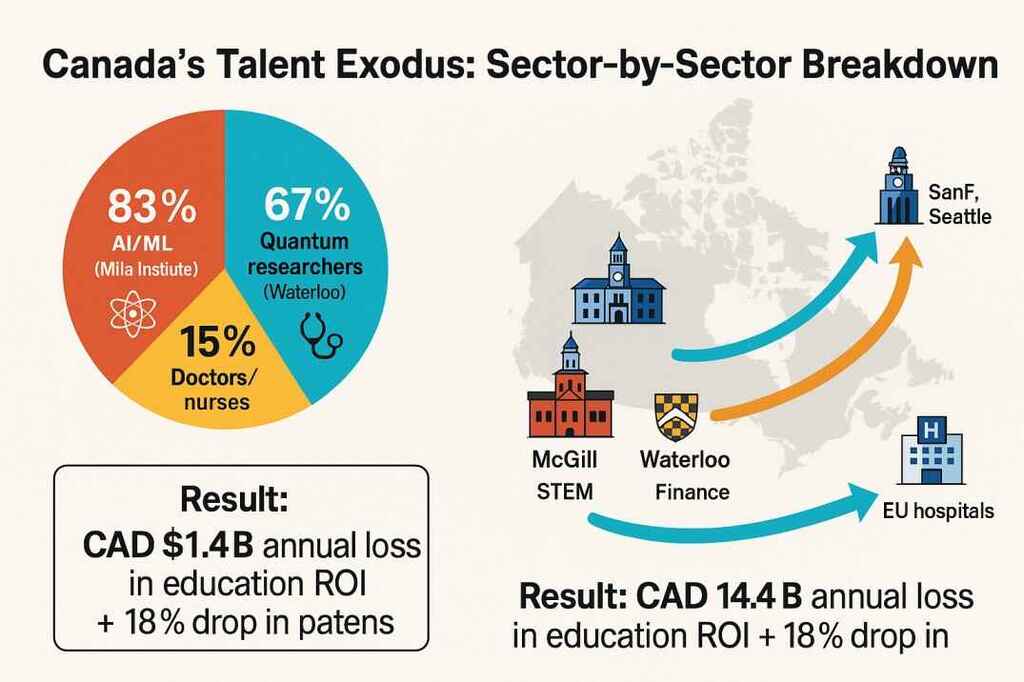

72% of STEM postgraduates from top schools like the University of Toronto and University of Waterloo relocate internationally within five years.

Average salary for software engineers: CAD $98,000 in Toronto vs. CAD $210,000 in San Francisco/Seattle (adjusted for cost of living).

83% of graduates from Montreal’s Mila Institute in AI/ML accept jobs abroad.

67% of researchers from Waterloo’s Institute for Quantum Computing are recruited by U.S. firms.

These disparities have real economic consequences. Since 2020, Canada has seen a 22% decline in AI patent filings, a key metric of Canadian innovation output.

Canada’s Talent Exodus: Sector-by-Sector Breakdown "A visual dive into where Canada's brightest go and why it’s costing the nation billions

Global Talent Retention: How Canada Compares

Canada’s brain drain challenge is stark when viewed in international context:

Germany retains 85% of its STEM graduates through robust university-industry ties.

TheU.K.loses 10% of its nurses annually but counters with aggressive visa incentives.

China, once a net exporter of talent, now reverses its trend with targeted R&D programs and the Thousand Talents initiative.

Africa loses 20% of its educated workforce, though largely due to instability, not policy failure.

Canada’s unique problem lies in the disproportionate loss of high-value talent, especially in AI, quantum computing, and biotech, which are essential to future economic competitiveness.

Beyond Tech: Other Sectors Hit by Talent Flight

The Canadian brain drain extends beyond STEM:

Healthcare: Canada loses 15% of trained doctors and nurses to the U.S. and Europe, worsening wait times and hospital understaffing.

Finance: Analysts and executives migrate to hubs like New York and London, where salaries outpace Toronto by nearly 50%.

Agriculture & Agritech: Innovators in sustainable farming are drawn to well-funded R&D centers abroad, impeding domestic advancements in food security and agricultural innovation.

These losses across sectors reveal a system-wide erosionof Canada’s human capital base.

Root Causes: Where STEM Policy Canada Falls Short

Key market and policy gaps continue to drive this tech talent migration:

Tax Disincentives

Marginal tax rates exceed 50% for high earners, compared to more competitive U.S. systems.

U.S. offers 401(k)s, better capital gains structures, and R&D tax credits that improve long-term earning potential.

Venture Capital Deficit

Canada sees only CAD $146 in venture capital investment per capita vs. CAD $483 in the U.S.

Nearly 90% of Canadian startups seeking Series B+ funding relocate to the U.S. to access capital.

Corporate R&D Shortfall

Canadian businesses invest just 1.6% of GDP into R&D, compared to 3.1% in the U.S.

This weakens the entire Canadian innovation ecosystem, making it hard to scale frontier technologies domestically.

The Innovation Drain Effect: Measuring Economic Impact

Direct Losses

Canada forfeits CAD $1.4 billion annually due to public education investments in students who then emigrate.

Indirect Impacts

Domestic patent filings have declined by 18% since 2015.

McGill’s Computer Science program fell 11 global ranking places.

Canada’s innovation economy risks stagnation as talent and ideas fuel foreign competitors instead.

Policy Solutions: Building a National Talent Retention Strategy

Solving the brain drain crisis requires coordinated action and bold reforms:

Short-Term (0–2 Years)

Talent Bonds: Offer student loan forgiveness for STEM graduates committing to five years of work in Canada.

Anchor Employer Incentives: Provide 25% payroll tax credits for firms that hire top-tier STEM talent.

Healthcare Retention Grants: Subsidize relocation and rural service bonuses for doctors and nurses.

Medium-Term (2–5 Years)

Boost VC Access: Double Canada’s per capita VC to CAD $300 via public-private funds.

Raise Corporate R&D Spending: Target 2.5% of GDP using tax credits and innovation incentives.

Align Education with Jobs: Re-tool academic curricula to reflect actual hiring needs in finance, healthcare, and agritech.

Long-Term (5–10 Years)

Tax Modernization: Lower marginal rates for high earners and align with global norms.

Sectoral Retention Frameworks: Establish targeted retention strategies for AI, quantum computing, and biotech (note: any export controls must be ethical and transparent).

Global Talent Hub: Create immigration fast-tracks to retain international graduates and build a sustainable pipeline of high-skill workers.

Pathforward: A Defining Choice for Canada’s Future

Canada’s STEM talent exodus is no longer anecdotal, it’s a structural crisis. The country now faces a defining choice: reform its STEM policy, R&D environment, and talent infrastructure or accept the role of a training ground for the world’s innovation superpowers.

As the Ottawa Science Policy Network puts it, “conducive policy changes are essential to building an environment where Canadian talent chooses to stay.”

Unless bold, coordinated action is taken, Canada risks losing the very minds it invests so heavily to educate, and falling behind in the global innovation race.

Why Africa Trades With The World But Not Itself: The...

Africa Business

At Addis Ababa’s gleaming terminal, two lines tell Africa’s story: one for Africans flying out (to Paris, Dubai, New York), another for foreigners flying in (mining deals, aid work, contracts). Rarely do you see Africans queueing to visit other African capitals as traders or tourists.

This isn’t about passports, it’s about economic absurdity. A Senegalese entrepreneur faces more hurdles selling to Nigeria than to France. Africa’s brightest measure success by how far they escape the continent. "Made in Africa" remains a novelty, not a norm.

Africa has the resources, demand, and demographic heft to thrive. What’s missing? The collective muscle memory to harness them.

The Cost of Fragmentation: Paying the Price of Smallness

The Addis airport lines aren’t just symbolic, they’re a receipt. A receipt for the fragmentation tax all Africans pay. Consider these contradictions:

Trade → Ethiopia imports steel fromChina cheaper than from South Africa (Afreximbank 2023).

Healthcare → Africa spends $2B/year training doctors who then staff European hospitals, while 1 in 3 clinics on the continent has no physician (WHO).

Travel → Only 4 African nations offer visa-free entry to all Africans. For comparison, Americans visit 13–30 African countries visa-free.

Infrastructure → Zambia’s copper exports still route through Dar es Salaam, not Namibia’s closer ports.

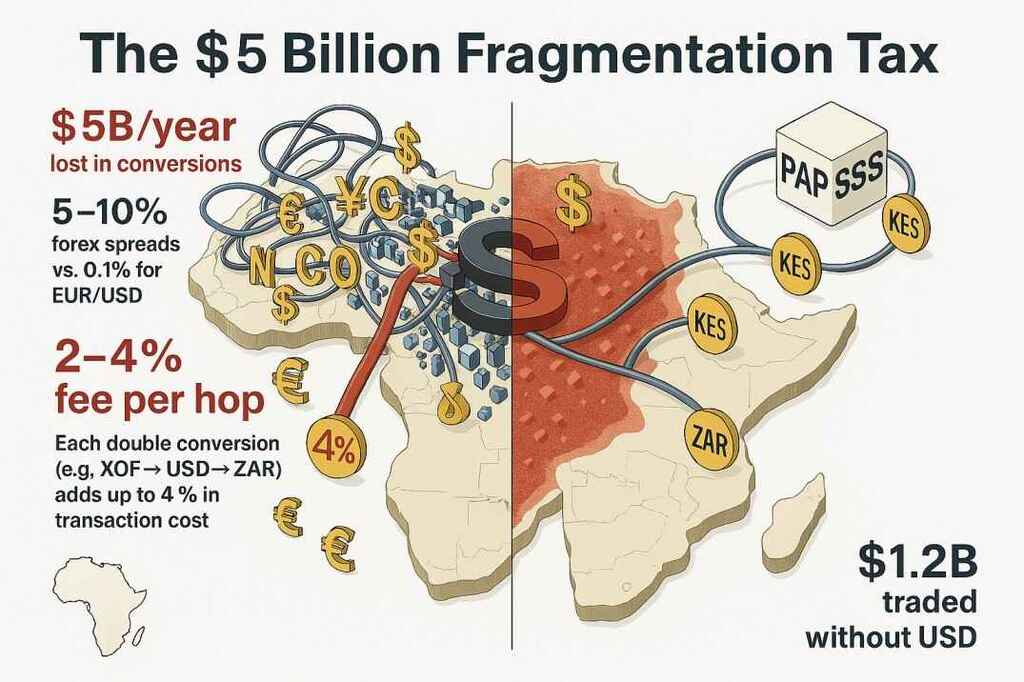

Digital → Internet traffic between Lagos and Accra (450km) detours 7,000km through Europe (Afrinic). Forex → $5 billion/year is lost by 42 African nations in currency conversions (Afdb).

Africa pays a $5B annual “fragmentation tax” due to costly currency conversions, double exchanges, and forex spreads up to 10%

How Currency Fragmentation Strangles Forex Markets

Africa’s 40+ currencies,many illiquid, non-convertible, or artificially pegged, create a forex market nightmare:

1. Liquidity Deserts & Painful Spreads

Most African currencies trade in thin markets, with bid-ask spreads 5-10x wider than EUR/USD.

Case Study: A Ghanaian importer buying Kenyan goods loses 7% upfront on shilling-cedi conversions (Ecobank).

2. Dollar Dependency = Free Money for Intermediaries

Intra-African trade often requires double conversions(e.g., XOF → USD → ZAR), adding 2-4% fees per transaction.

Parallel Markets: In Nigeria, the naira’s black-market rate trades 40% below official rates (IMF 2023).

3. Central Banks on Life Support

Low Reserves: 60% of African central banks hold <3 months of import cover, leaving currencies vulnerable to speculative attacks.

Case Study: Ghana’s cedi collapsed 50% in 2022 after reserves dried up.

4. No Hedging = Investor Flight

OnlySouth Africa, Egypt, Kenya have liquid currency futures. Others face 8-12% hedging costs (vs. 1-3% in developed markets).

Result: Foreign investors demand higher returns to compensate forunhedgeable risk.

Colonial Logistics, Modern Consequences

Africa inherited borders that make zero logistical sense. The damage?

Ports: 73-78% of port capacity is foreign-controlled (China owns 19-23%).

Trucking: A Mombasa-Kampala haul spends 18 hours at borders, longer than the actual drive (TMEA).

Airlines: African carriers fill 62% of seats on continental routes vs. 82% on Europe-Africa flights (IATA).

Informal Trade: 38-42% of intra-African commerce happens off the books (UNCTAD).

The ultimate irony? When COVID hit, Africa created a mutual health passport system in 9 weeks.

Proof:Integration is possible when lives depend on it.

Where the Rubber Meets the Road: Solutions in Action

While AU summits gather dust, three movements are bypassing bureaucracy:

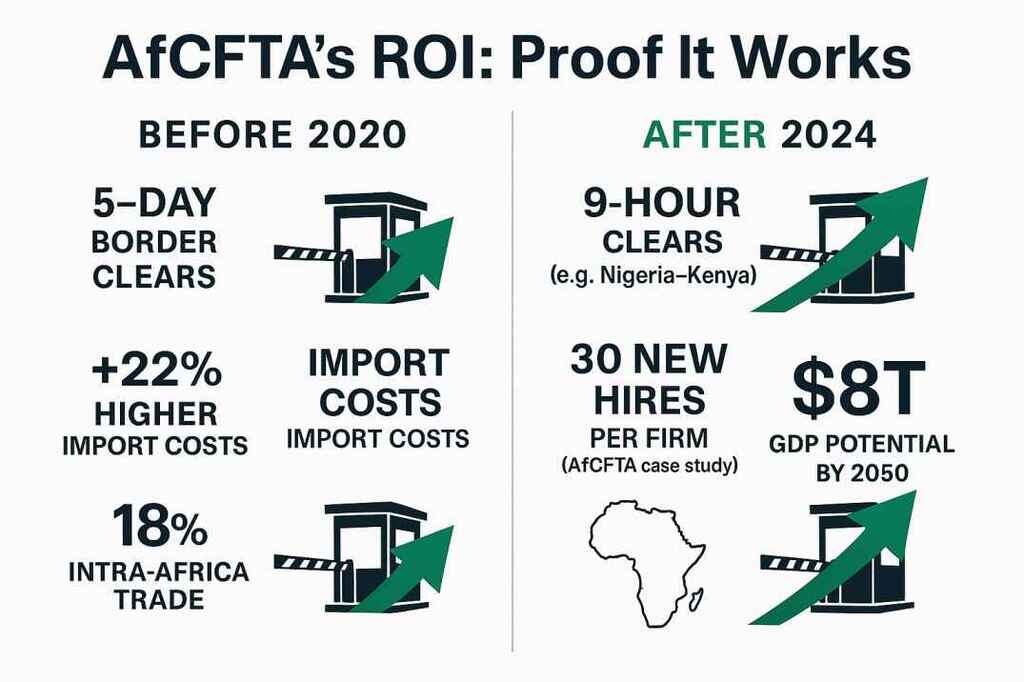

1. AfCFTA’s Quiet Revolution

The African Continental Free Trade Area is already cutting costs:

Nigerian firms slashed parts imports from Kenya by 22%.

Border clearance times fell from 5 days to 9 hours in pilot corridors (AfCFTA Q2 2024).

2. Fintech’s Forex Rebellion

PAPSS: Cleared $1.2B in trade without touching the dollar.

Lori Systems: Uses AI to cut border delays in 11 countries.

Africa Data Centres: Locally routes 38% of intra-African internet traffic.

From 5-day delays to 9-hour clears. AfCFTA is breaking barriers and fueling Africa’s $8T GDP dream, cutting import costs by 22%, driving intra-African trade from 18%, and creating 30 jobs per firm. Trade’s getting faster, smarter, and stronger

The $8 Trillion Stakes (By 2050)

Africa’s GDP could hit $16 trillion, but only if intra-African trade rises from 18% to 50%. The gap? $8 trillion in lost prosperity.

Who Must Act?

Governments:

Ratify AfCFTA Phase II (47/54 nations are stalled).

Roll out the African Passport by 2025.

Deploy armed trade corridor escorts (not just peacekeepers).

Businesses:

Dangote Cement added $1.3B revenue by prioritizing regional expansion.

MTN’s $1B fiber network cut West African data costs by 60%.

Citizens:

Demand visa openness (Rwanda’s policy created 150,000 jobs).

FixTheCountry movements (like Ghana’s) forced port reforms.

Bottom Line: The Clock is Ticking

Kwame Nkrumah warned in 1963: "Unite or perish." Today, it’s unite or stagnate. The tools exist. The models work. The only question: Will leaders lead, or will they be outpaced by the entrepreneurs and engineers already building the future?

Final Answer: Africa’s economic fragmentation isn’t fate, it’s a series of solvable problems. The first step is admitting the receipt it has been handed is too damn high.

Europe’s Gig Economy Split [2025 Data]: 43 M At €15/Hour...

Europe Business

Imagine a Lisbon coder rocking Upwork from a sunlit café, or a Berlin courier weaving through the streets with a Deliveroo order. Europe’s gig economy is no longer a side hustle, it’s a multi-billion-euro driver of flexible work, reshaping the continent’s labor landscape with just a tap on a smartphone.

The Platforms Powering Europe’s Freelance Boom

Digital platforms like Fiverr, Deliveroo, Bolt, and Upwork are turning smartphones into on-demand job hubs, matching talent to work in seconds, whether it’s designing logos in Milan or delivering lunches in London.

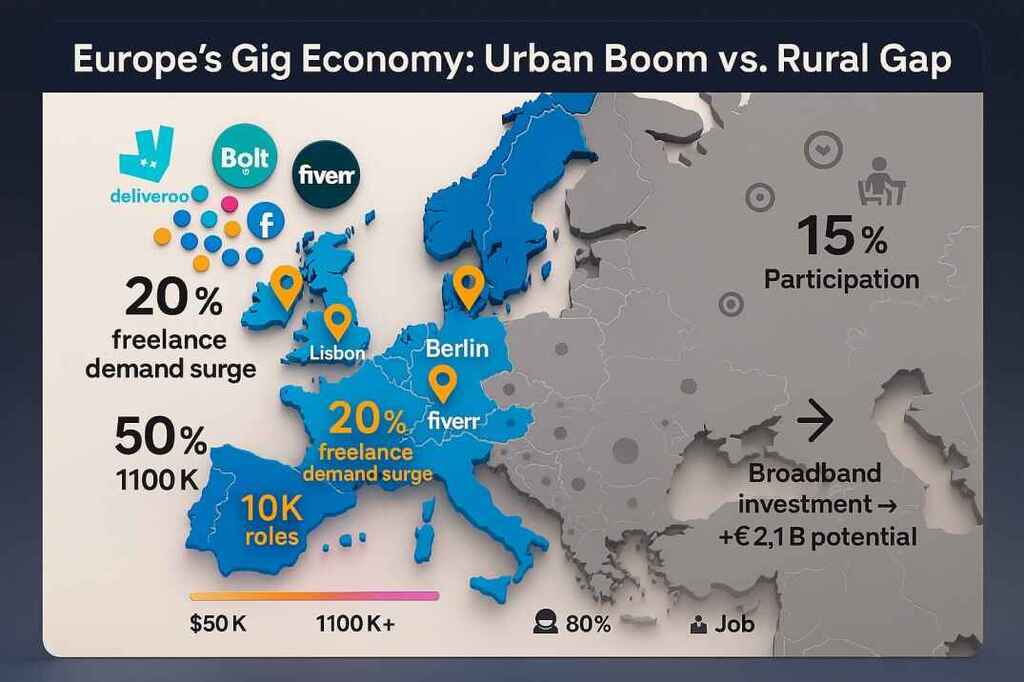

The platform workforce grew from 28.3 million in 2022 to an estimated 43 million by 2025(Littler Mendelson P.C.)

Cities like Berlin and Lisbon have 20% jumps in freelance demand, with fewer than half of those workers earning over $50,000, and just 13% crossing $100K annually.

City Lights vs. Village Nights: The Urban–Rural Gig Divide

The digital divide is stark:

70% of freelancersare under 35 and based in cities; only 15% of rural workersparticipate in gig platforms, with 80% still preferring traditional employment (World Bank).

Rural freelancers face slow internet, limited digital confidence, and social expectations tied to traditional work.

Elena, a freelance copywriter in rural Hungary, shares: "Bad Wi‑Fi kept me offline for months, only after NGO training did gigs become reliable."

But there’s hope: investing inbroadband access, localized digital training,and community co-working hubs could unlock huge untapped potential outside urban centers.

From Lisbon’s laptops to rural buffer zones: Europe’s gig economy surges past 1100K roles, yet broadband gaps risk leaving remote talent behind as cities rake in €2.1B through platforms like Deliveroo and Fiverr.

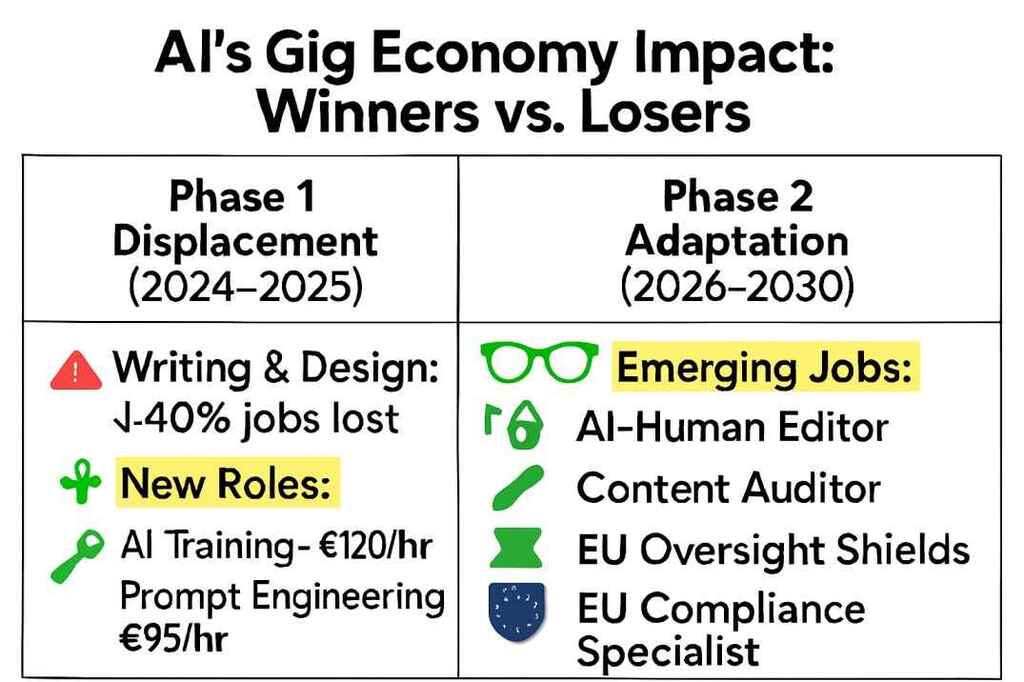

AI in the Driver’s Seat: Reinventing the Gig Workforce

Artificial Intelligence is shifting the gig job landscape:

High-income roles like AI prompt engineering and model training are now paying up to €120/hour.

Anna, an Amsterdam-based designer, explains: "Three clients vanished to AI tools in 2024. I had to pivot to AI-prompted design to stay competitive."

This is fueling a new "tech elite" among freelancers. and sidelining those without upskilling opportunities.

AI Reshapes the Gig Game: Writers and designers face early losses, but high-paying roles like Prompt Engineers and EU Compliance Specialists rise as the new frontier

Fairness in the Algorithm Age: EU Rules in the Mix

In December 2024, the EU enacted the Platform Work Directive (EU 2024/2831):

It legally presumes gig workers are employees under platform control, granting them rights to benefits and human oversight of automated decisions (Taylor Wessing, Crowell & Moring).

Member states must transpose the law by December 2026.

Yet problems persist:

54% of workers lack benefits like health insurance and paid leave.

38% earn between $10–$14.99/hour, whilewomen earn 18–23% less (Taylor Wessing).

The Persistent Gender Pay Gap: Why Women Earn Less in the Gig Economy

While the platform economy promises equal access, data reveals entrenched disparities: 18-23% earnings gap persists across major platforms (Taylor Wessing, 2024).

Structural causes:

Algorithmic bias:Platforms prioritize "reliability metrics" that disadvantage women with care responsibilities.

Gig segregation: Women cluster in lower-paid care/service roles while men dominate tech/transport.

Bargaining disparity: Male freelancers negotiate rates 25% more often (Upwork internal data).

Motherhood penalty: Algorithms interpret childcare gaps as "low availability".

Case Study: Uber's Successful Adjustments Uber UK's 2022 reforms narrowed their gender earnings gap by 8% through:

Blinded trip assignments: Removed driver gender from dispatch algorithms.

Flex+ program: Paid waiting time for drivers with care responsibilities.

Dynamic pricing caps: Limited surge pricing on school/hospital routes.

Location-based bonuses intended to help women actually rewarded male cyclists in wealthy urban areas (LSE study, 2024).

Peak-hour quotas for female riders led to account sharing with male partners.

Customer tipping bias persisted, with male riders receiving 19% larger tips (Deliveroo internal data).

Key Lessons Emerging:

Simple fixes fail: Gender-neutral algorithms often perpetuate existing biases.

Local context matters: Solutions must address regional work patterns.

Transparency is crucial: Workers need to understand how pay systems function.

Policy Solutions Gaining Traction:

France's 2023 "Gig Equity Law" now requires bias testing before algorithm updates.

Berlin's revised "Fair Crowdwork" program ties funding to verifiable pay equity gains.

EU Directive Article 12 amendments will audit platform interventions annually.

Platform workers across France, Italy, and Germany are mobilizing, calling for algorithm transparency, fair pay, and legal protections.

Strategic Roadmap: Tailored Actions for the Gig Economy’s Future

To sustain the momentum and build a fair, inclusive, and scalable future for gig work in Europe, key stakeholders must align their actions across specific time horizons:

For Platforms Short Term (0–2 years):

Improve algorithm transparency and simplify how pay is calculated.

Introduce baseline pay guarantees and dispute resolution tools.

Medium Term (3–5 years):

Localize platform infrastructure to better serve rural and underserved regions.

Launch skilling and certification programs in high-demand digital tasks (e.g., AI labeling, UX design).

Long Term (6–10 years):

Develop hybrid platform ownership models that offer equity or dividends to workers.

Integrate benefit systems (healthcare, pensions) directly into platform ecosystems.

For Investors

Short Term (0–2 years):

Invest in platforms with strong ESG alignment, labor transparency, and early compliance with EU regulations.

Prioritize gig startups focused on financial inclusion, fair pay, and algorithmic accountability.

Medium Term (3–5 years):

Back ventures expanding into rural gig markets or developing AI-integrated freelance ecosystems.

Support platforms offering portable benefits and career progression frameworks.

Long Term (6–10 years):

Fund platforms pioneering cross-border labor solutions and multi-sector gig ecosystems.

Encourage industry coalitions or investment vehicles that promote ethical AI use in labor matching and compensation.

For Policymakers

Short Term (0–2 years):

Begin transposing the 2024 EU Platform Work Directive into national law.

Conduct regulatory audits on platforms to enforce worker rights, data use transparency, and pay equity.

Medium Term (3–5 years):

Build an EU-wide framework for portable benefits, including sick leave, retirement, and unemployment insurance.

Incentivize digital infrastructure in rural areas to close participation gaps.

Long Term (6–10 years):

Regulate AI and automated decision-making systems used by gig platforms.

Harmonize platform labor laws across the EU to prevent a “race to the bottom” in worker protections.

For Gig Workers Short Term (0–2 years):

Join digital worker cooperatives or forums for legal support and bargaining power.

Track income and hours to evaluate the sustainability of gig work and prevent burnout.

Medium Term (3–5 years):

Reskill in growth areas like AI prompt engineering, remote IT support, or project management.

Explore creating personal brands and client rosters for more stable freelance income.

Long Term (6–10 years):

Participate in shaping digital labor laws through advocacy or citizen assemblies.

Transition into portfolio careers, combining gig work, consulting, and passive income streams.

A Stakeholder's Summary of Strategic Recommendations over the Short-term, Medium term and Long term

By aligning on this strategic roadmap, stakeholders can unlock the full potential of the European gig economy, ensuring it remains flexible, inclusive, ethical, and built for long-term resilience.

The Road Ahead: Will Europe Level the Gig Playing Field?

Europe’s gig economy is no fringe phenomenon, it’s becoming mainstream. But the future hinges on whether digital opportunity is inclusive and fair:

Will rural communities gain real access?

Can regulation keep up with platform innovation?

Will tech-driven inequalities be addressed before they widen?

Europe can still shape a future where flexible work is not just scalable, but equitable,but only if it invests wisely in people, technology, and policy.

The gig economy is here. But the question remains: will it work for everyone?

South America’s $15 T Digital Revolution: Fintech, Ag Tech &...

SouthAmerica Business

The market landscape in South America is rapidly changing. Imagine tech-driven agriculture, digital currencies, record-breaking trade agreements, fast-moving e-commerce, and significant investment interest. However, there are layers to the market—national, regional, and international—so it's not all plain sailing. This article explores the major growth drivers, risks, and strategic recommendations for key stakeholders.

Latin America’s E-Commerce & Fintech Explosion: Who’s Leading and Why It Matters

E-commerce and digital finance are revolutionizing South America’s economy, creating new powerhouses and investment magnets across the region.

MercadoLibre, often dubbed “Latin America’s Amazon,” smashed expectations: Q1 net profit surged 44%, revenue jumped 37%, with Mercado Pago driving payment and credit services growth.

Fintech boom continues: Revolut acquired Cetelem Argentina (BNP Paribas) to access cross-border banking. Ualá, Clip, and Mercado Pago also compete in this high-growth space.

Digital payments are mainstream:

Brazil’s Pix handles ~40% of online transactions, used by 75% of adults.

Regional fintech market reached $889b in 2023 with a 39.4% CAGR forecast through 2032.

AgTech & AgFintech in South America: How Innovation is Transforming Farming

Agriculture remains the backbone of South America, but agtech and agfintech are redefining how it works.

Brazil leads in soy, coffee, beef; Colombia in avocado, cocoa, and sugarcane.

Small farmers face credit challenges. Agfintech solutions include:

Traive: Uses AI to assess farm credit risk; raised US$20M from Banco do Brasil.

Solinftec: Robotics + AI agtech firm backed by TPG and Bloomberg-linked investors.

These innovations enhance productivity and promote financial inclusion.

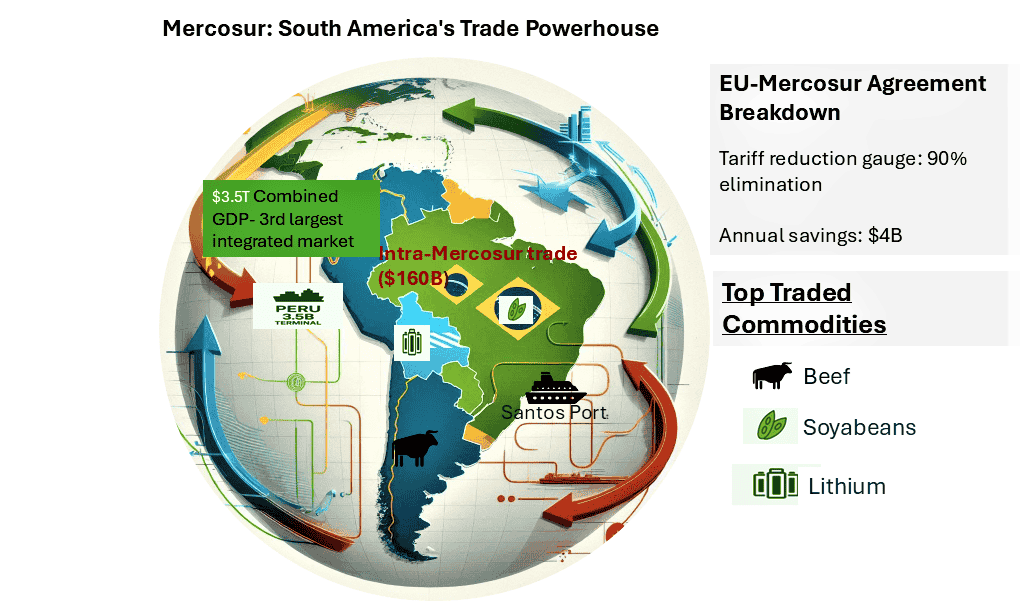

Mercosur Trade and the EU Deal: Unlocking a $4 Billion Opportunity

South America's regional trade networks are strengthening with global momentum, particularly through Mercosur and new international agreements.

Mercosur: Brazil, Argentina, Paraguay, Uruguay, and Bolivia form the 3rd-largest integrated market ($ 3.5t GDP, $160b intra-bloc trade in 2023).

EU-Mercosur Agreement: Pending deal to eliminate tariffs on 90% of goods, affecting 780 million people and 25% of global GDP (European Trade Commission).

China's footprint grows: Investments in Brazil’s Port of Santos and Peru’s $3.5 b deep-water terminal deepen South America’s global integration.

EU–Mercosur Pact: $4B Tariff Cuts, Strategic Port Investments & Commodity Powerhouse Drive $160B Trade Flow Across $3.5T Market.

Open Finance in South America: The API Revolution Reshaping Banking

Open banking and API-based finance frameworks are unlocking digital ecosystems and empowering small businesses across Latin America.

Brazil: Rolled out open finance APIs.

Chile: Passed fintech and financial portability laws.

Colombia & Ecuador: Building robust regulatory frameworks.

Informal workforce exclusion from digital finance.

Environmental degradation tied to mega-infrastructure.

Ethical Imperatives:

Policymakers must enforce ESG frameworks.

Investors should adopt sustainability metrics.

Entrepreneurs must co-create inclusive tech with communities.

South America Market Forecast 2025–2032: Where the Smart Money is Going

Future trends show explosive potential across multiple sectors but long-term winners will prioritize sustainability, scale, and inclusion.

Fintech: Market projected to hit US$15 t by 2032 (CAGR ~40%).

AgriTech: AI-powered lending, robotics, and data-led agronomy will redefine farm output and inclusion.

Trade: EU-Mercosur could unlock US$4 b in annual savings.

Global Influence: China’s port and agri-investments reflect deepening ties.

Policy, Investors & Entrepreneurs: Strategies to Win in Latin America’s Growth Wave

To fully unlock South America's potential, each stakeholder group must take targeted, time-bound action.

Policymakers:

Harmonize digital regulations regionally.

Build rural digital infrastructure.

Create ESG-aligned investment incentives.

Entrepreneurs:

Focus on localization and financial literacy.

Build solutions for informal and rural economies.

Co-design products with user communities.

Investors:

Short-Term (1–2 yrs): Focus on mature fintechs and digital payments (e.g., Pix, Mercado Pago).

Mid-Term (3–5 yrs): Fund agtech, open finance startups, cross-border e-commerce enablers.

Long-Term (6–10 yrs): Bet on infrastructure, regional trade platforms, and ESG-driven ventures.

Bottom Line - Digital transformation in Latin America

South America’s markets are creative and powerful, driven by booming fintech, smart agriculture, integrated trade, and tech-savvy ecosystems. While not without its issues (infrastructure, instability, bureaucracy), the direction is momentum-driven.

With the right blend of innovation,inclusive design, and resilient policy, South America may very well be the world’s next major growth engine.

South America 2025: Democracy Under Fire As Conservative Wave Clashes...

SouthAmerica Politics

The political landscape of South America in 2025 resembles a high-stakes drama: plot twists, unexpected outcomes, and relentless tension. From Javier Milei’s libertarian overhaul in Argentina to mounting protests in Colombia and a wave of conservative momentum across the region, the continent is undergoing a seismic shift. But this is not a story of collapse, it’s one of transformation. South America remains a battleground where democracy, reform, and activism collide with populism, inequality, and instability.

South America’s Right Turn: Reformers or Authoritarians in Disguise?

Across Latin America, a center-right resurgence is gaining ground but this isn’t a return to dictatorship or radical populism. Instead, it's fueled by economic discontent and demand for order.

Argentina's President Javier Milei, elected in late 2023, slashed public spending by over 50% in his first six months, according to Bloomberg. His use of executive decrees over 100 in 2024 alone, has drawn criticism from the Center for Legal and Social Studies (CELS) over judicial independence concerns (Bloomberg).

In Ecuador, President Daniel Noboa, elected in 2023 at age 36, renewed multiple nationwide states of emergency to combat gang violence. While public support remains above 60% (El Universo, June 2025), democratic watchdogs like Fundamedios warn of a dangerous normalization of emergency rule.

Chile’s conservative candidate Evelyn Matthei leads 2025 presidential polls with 38% support (Cadem, July 2025), signaling a shift away from Gabriel Boric’s progressive coalition. This conservative wave reflects frustration with inflation, corruption, and insecurity. Yet most new leaders remain within democratic bounds, favoring free-market reforms over ideological extremism.

Fighting Back: How Social Movements and Courts Are Defending Democracy

Even as center-right leaders gain power, democracy across South America isn’t eroding, it’s evolving. Brazil’s President Luiz Inácio Lula da Silva, now in his third non-consecutive term, has reversed over 30 Bolsonaro-era executive actions, including environmental deregulations and restrictions on civil society groups. Brazil is also hosting COP30 in Belém, positioning itself as a global environmental leader (Reuters).

Feminist and Indigenous movements continue driving progressive agendas. In Colombia, activists recently won a constitutional court ruling to protect Indigenous land rights in the Amazon basin.

Abortion rights are advancing across the continent: Mexico, Argentina, Colombia, and most recently Uruguay, have expanded access since 2020. LGBTQ+ protections are also slowly strengthening, even under conservative governments like Ecuador and Chile. Despite institutional strain, South American democracy is being actively defended not just by leaders, but by the people.

Election Earthquake: Why 2025 Will Redefine Latin American Power

With elections across Latin America this year, the region is in electoral overdrive, and tensions are rising.

In Peru, President Dina Boluarte’s approval stands at 4% (Ipsos, July 2025), with widespread unrest over corruption scandals and rising crime. Constitutional reforms have stalled amid parliamentary deadlock.

Colombia’s President Gustavo Petro, elected in 2022, is under fire after his healthcare and pension reforms were blocked. In response, over 47 mass protests have occurred across 33 municipalities since March 2025, disrupting transit and sparking strikes (Aljazeera- Colombia Protests).

In Ecuador, Noboa’s anti-gang campaign has arrested over 20,000 suspects since January (El Comercio), but violence persists fueling debate over the balance between security and democracy. This year’s election outcomes will define the next decade of governance, democratic resilience, and global alignment for the region.

New Cold War in the South? Latin America Navigates Between China and the U.S.

Latin America is becoming an increasingly strategic player in global politics. Brazil hosting the BRICS summit 2025 and COP30, reflects its ambition to lead in both climate diplomacy and alternative global governance structures.

Under Donald Trump’s second term, the U.S. has revived Monroe Doctrine-style rhetoric, threatening to curb Chinese infrastructure and tech investments in Latin America.

Ecuador, which sends over 35% of its exports to China, has warned that cutting ties under U.S. pressure would be a “trade disaster,” according to Foreign Minister Gabriela Sommerfeld (June 2025 press briefing).

Simultaneously, countries like Chile and Paraguay are courting both European Union green funds and Belt and Road initiatives, hedging between East and West. This multipolar moment forces South American leaders to recalibrate their alliances carefully while protecting domestic interests.

A $15B tug-of-war for Latin America’s soul, where the U.S. fortifies borders, China builds trade routes, and the EU bets on climate diplomacy. In 2025, South America stands at a crossroads of global influence and regional identity.

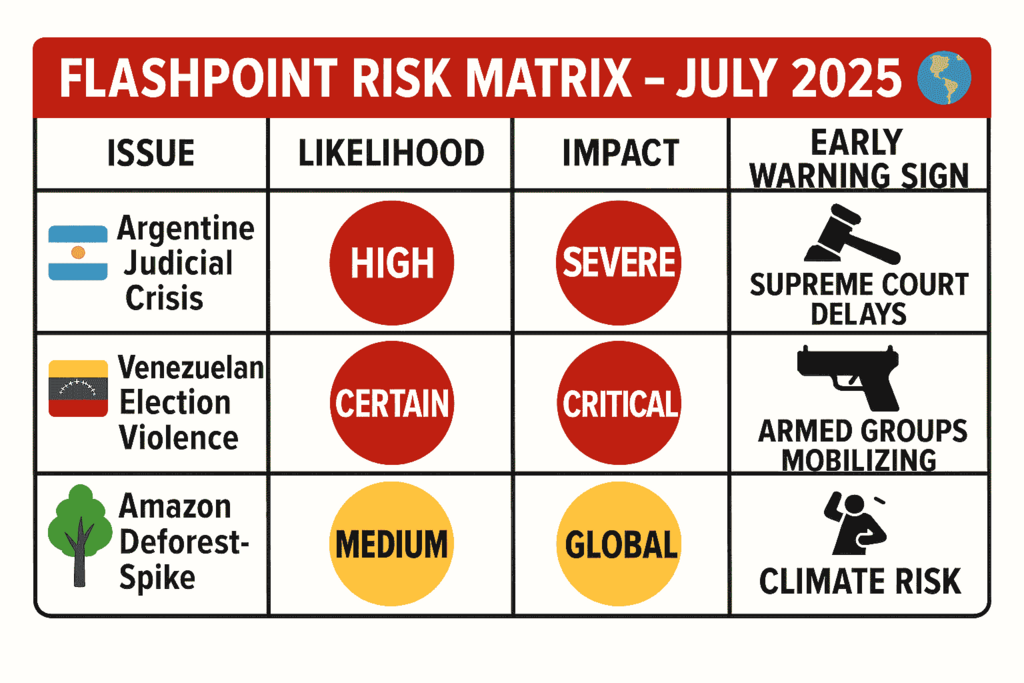

Crisis Watch: Where Things Could Erupt Next in South America

Key political and social flashpoints could shift regional trajectories: Judicial independence: Milei’s aggressive judicial reforms and court appointments are under review by Argentina’s Supreme Court. Analysts warn of “institutional fatigue” (Universidad Torcuato Di Tella).

Authoritarian pressure: Venezuela’s 2025 presidential elections remain tightly controlled under Maduro, with international observers partially banned. Bolivia’s judicial disputes and Ecuador’s emergency decrees also remain points of concern.

Social unrest: Colombia’s strikes, Peru’s crime surge, and economic frustrations in Paraguay and Uruguay indicate public patience is wearing thin.

Climate accountability: COP30 in Brazil brings global focus to Amazon deforestation, El Niño droughts, and whether climate promises will meet action, or stall under political pressure.

South America's 2025 flashpoints, where fragile courts, embattled elections, and vanishing forests converge in a storm of democratic strain, ecological urgency, and geopolitical consequence.

South America 2025: Chaos or Comeback? The Battle for the Region’s Soul

South America in 2025 is not descending into chaos, but it is navigating a complex, high-pressure transformation. The continent is witnessing:

A conservative revival that is reshaping economic policy and governance.

A grassroots defense of democracy, led by civil society, social movements, and watchdog groups.

A foreign policy recalibration amidst U.S.-China competition.

An electoral cycle that could redefine the democratic map of the region.

Key questions remain:

Will executive overreach be checked by courts and congresses?

Can social movements sustain their momentum?

Will leaders act on climate or fall into performative politics?

Can countries maintain sovereignty in an increasingly polarized global arena?

South America isn't a passive stage, it’s an active player in shaping 21st-century democracy, geopolitics, and sustainability. As the region evolves, one thing is certain: Ignore South American politics at your own risk. The future of the hemisphere may just be written here.

A leading global company for Business Solutions , bringing the intriguing global business arena into your space to a business and financial savvy mind.

social media:

Stay In Touch

Don't hesitate. Reach us with these info.

0795046415financialshub01@gmail.comNairobi/Kenya

We create great content everyday. Subscribe to be the first notified when released.

.jpg)

.jpg)

.png)