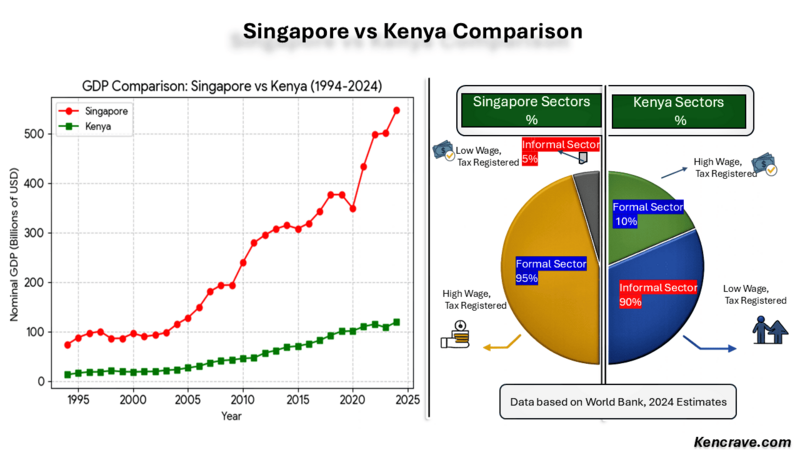

Singapore vs Kenya economic comparison visual showing GDP growth from 1994-2024 and formal vs informal sector breakdown. Image Credits: Kenneth Njoroge via Kencrave.

Africa

Executive Summary

Kenya and Singapore started at the same GDP in 1963. By 2023, Singapore reached $500B; Kenya stayed at $113B. The difference is not resources, t's institutions that outlast elections.

As Kenya approaches the 2027 elections and beyond, politicians promise "Singapore-style" growth. But without election-proof reforms, an independent civil service, a 15-year Investment Protection Pact, and incentive-based formalization of an estimated 90% informal workforce, these promises will fail. Singapore Dream vs. Kenya's Reality: Can 2027 Elections Deliver Long-Term Growth?

Can Kenya become like Singapore?

Kenya cannot directly replicate Singapore’s economic model due to differences in size, governance, and political systems. However, Kenya can achieve long-term economic growth by strengthening institutions, ensuring policy stability beyond election cycles, and gradually formalizing its large informal sector.

The “Singapore Dream” in Kenya’s 2027 Elections

As Kenya approaches the 2027 elections, its political leaders are once again promising swift economic change, often describing it as a future similar to Singapore's. The idea is appealing, but the real challenge lies in institutions.

Kenya's five-year election cycles often shift policy goals, unlike Singapore, where growth depended on long-term, stable institutions protected from political changes. The key question for 2027 is whether Kenya can develop strong enough institutions to survive beyond election cycles, rather than simply copying Singapore’s model.

The phrase “Singapore-style” now symbolizes order, discipline, and stability in campaigns. While Singapore’s success is often attributed to visionary leadership under Lee Kuan Yew, its true foundation was policy continuity, administrative efficiency, and long-term planning.

Kenya’s development plans are frequently changed, delayed, or halted after elections, making this a governance issue as much as an economic one. Investors value predictability, and voters care about actual results.

Why Kenyan Politicians Compare Kenya to Singapore

As Kenya's 2027 elections draw closer, the Singapore narrative serves multiple political purposes:

A promise of economic transformation: Singapore represents order, efficiency, and prosperity which an appealing contrast to Kenya’s current challenges of high living costs, unemployment, and rising public debt.

A tool for political contrast: By invoking Singapore, politicians indirectly criticize past governments without offering detailed accountability

A Rallying cry for tough reforms: Invoking Singapore helps justify tough reforms, or promises of them, by framing sacrifice as necessary for long-term gain. The message is simple: Endure now so the future can improve.

According to the latest World Bank’s Kenya Economic Update, the primary hurdles to Kenya's growth are not a lack of vision, but fiscal strain, rising debt-servicing costs, and policy volatility. The country faces an implementation gap. Policies often change when fiscal priorities shift. Since 2022, large debt repayments have reduced funds for development. The government has responded with higher taxes and spending cuts. These repeated policy adjustments create uncertainty and weaken long-term investment.

Why Singapore Succeeded Economically

Singapore’s rise was not sudden. It followed a clear, state-led road map over decades, anchored in policy continuity rather than in election cycles.

Timeline visual illustrating Singapore’s key economic and policy milestones from 1965 to the 2020s, including independence, industrial takeoff, global integration, and high‑income consolidation.

1965 Independence: Survival With no resources and high unemployment, the priority was basic state credibility. The focus was on housing, public health, and the rule of law. Growth was driven by establishing order.

1965-1975: Building an "Election-Proof" State Singapore built a professional, meritocratic civil service, paid competitively, and protected from political turnover. The Economic Development Board coordinated policy. Corruption was punished consistently. Investors trusted the rules before they trusted the returns.

1975-1985: Industrial Takeoff

With a functioning state, Singapore attracted multinationals into export manufacturing with clear, long-term tax and regulatory guarantees. Skills training was aligned with industrial needs.

1985-1997: Upgrading the Economy As wages rose, planning shifted to higher-value activities in finance, logistics, and advanced manufacturing through targeted education reform and sectoral policies.

1997-Present: Knowledge Economy After the Asian Financial Crisis, Singapore doubled down on resilience, expanding into biotech and tech. Large fiscal reserves and institutional continuity carried the economy through shocks. Today, challenges are inequality and productivity, but policy shifts remain incremental.

The difference:This continuity came with trade-offs: restricted political dissent and a centralized, city-state model. Kenya’s path must reconcile long-term planning with democratic accountability, devolution, and a vast informal sector.

Line graph comparing Singapore and Kenya GDP from 1963 to 2023, highlighting major economic events such as independence, recessions, financial crises, and COVID‑19.

Observations from the Graph:

1963 to 1965, same starting point. In 1963, Kenya’s GDP was about 927 million dollars. Singapore’s GDP stood at 918 million dollars. Both countries were former British colonies. Each faced weak infrastructure, low literacy, and little industrial capacity.

Late 1960s to 1970s, policy divergence . Singapore, under Lee Kuan Yew, adopted export-oriented industrialization and opened the economy to foreign direct investment. Kenya recorded a growth of about 6.6%, but relied on agriculture and import substitution policies that protected local industries.

1980s to 1990s, different outcomes. Kenya experienced slow growth, political instability, and rising corruption. Economic reforms under structural adjustment created pressure on public spending. Singapore shifted from labor-intensive industries such as textiles to high-value sectors such as electronics and chemicals. The country built a strong manufacturing and technology base.

Recovery and disruption. Kenya entered a reform phase during the presidency of Mwai Kibaki. Infrastructure investment increased, and economic growth rose above 5 %. Singapore faced a short economic shock during the severe acute respiratory syndrome outbreak, SARS in 2003 but recovered quickly and strengthened its position as a global financial center.

2020 to 2023. New divergence. Both economies faced the shock of the COVID-19 pandemic. Singapore recovered faster due to its service-based and technology-driven economy. Kenya faced fiscal pressure linked to high public debt and a slower recovery.

Productivity gap. By 2023, Singapore’s GDP exceeded 500 billion dollars, while Kenya’s GDP was about 113 billion dollars. Kenya’s population is close to 55 million. Singapore has about 5.9 million people. The difference shows how higher productivity and high-value services drive output.

Policy over resources. Singapore has almost no natural resources. Strong institutions, investment in education, and a predictable business environment supported growth. Policy choices shaped outcomes more than resource endowment.

Growth patterns. Kenya’s growth path shows cycles of expansion and slowdown. Singapore’s growth accelerated sharply after the 1980s as it integrated into global trade and finance.

Income gap. Kenya reached lower-middle-income status in 2015. Singapore is a high-income economy. GDP per capita in Singapore exceeds 80,000 dollars, while Kenya’s is estimated at 2,200 dollars.

Stacked bar chart comparing the 2025 middle class effective tax burden between Kenya (32.1%) and Singapore (24.5%), showing income tax, social security, and health/housing levies as a percentage of monthly gross income.

Middle Class Effective Tax and Cost Burden, 2025

This comparison looks at a typical middle-income professional in each country.

Kenya's total burden is about 32.1 % A worker earning about 150,000 Kenyan shillings per month faces a large deduction from payroll taxes. Income tax through Pay As You Earn accounts for roughly 25 %. Mandatory contributions to the Social Health Authority, the Housing Levy, and the National Social Security Fund increase the total statutory deduction to about one-third of gross income.

Singapore's total burden is about 24.5 %

A worker earning about 7,000 Singapore dollars per month faces a lower overall deduction. The largest component is the Central Provident Fund contribution of about 20 %. This contribution works as a compulsory savings system. Individuals later use these funds for housing, retirement, and healthcare. Income tax for this bracket remains low, close to 4.5 %.

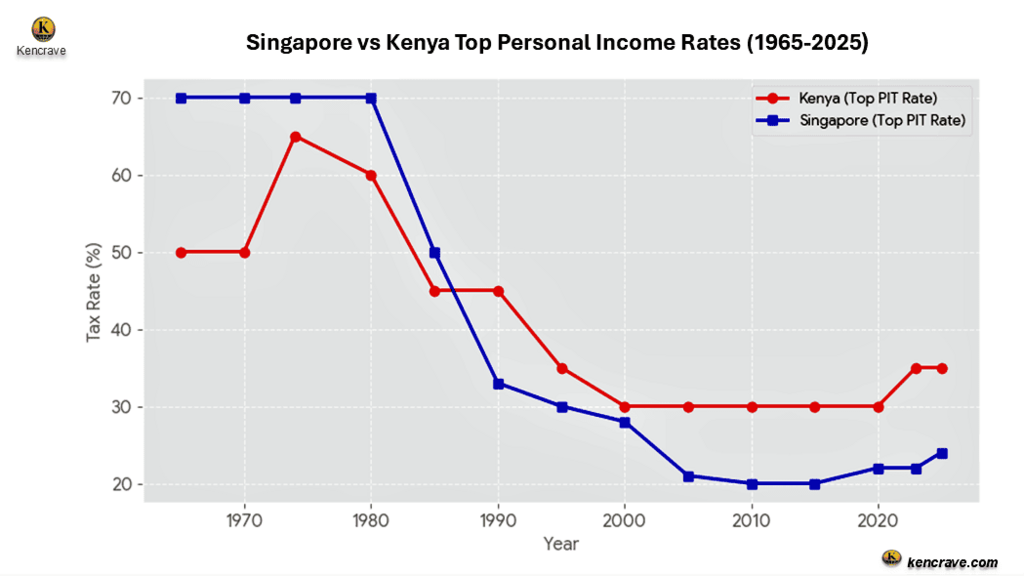

Historical Top Personal Income Tax Rates, 1965 to 2025

The below chart tracks the evolution of personal income tax rates after independence in Singapore and Kenya.

Line graph comparing historical top Personal Income Tax (PIT) rates in Singapore and Kenya from 1965 to 2025, illustrating a downward trend from 70% to current levels below 40% for both nations.

Singapore’s strategy In the 1960s and 1970s, Singapore set the top personal income tax rate at about 70%. Over time, the government cut the rate to attract skilled workers, investors, and multinational companies. The rate gradually dropped to 20%. In 2024, it increased slightly to 24%to address rising inequality while keeping the system competitive.

Kenya’s strategy Kenya also started with high rates. The top rate reached about 65 % in 1974. Later reforms reduced the rate and stabilized it at 30 % for close to two decades. In 2023, the government raised the top rate to 35 % as fiscal pressure increased and public debt payments grew.

Key Observations on economic differences (Singapore vs Kenya)

Tax versus savings: The biggest structural difference lies in how deductions function. In Singapore, most deductions go into the CPF and remain tied to the individual’s long-term savings and benefits. In Kenya, most deductions go into centralized government funds, which many taxpayers feel deliver fewer direct personal returns.

Recent policy divergence: Singapore maintains a stable and predictable tax structure. Changes happen gradually. Kenya has introduced several new deductions in a short period, including the Housing Levy and the Social Health Authority, while also raising the top tax bracket.

Public services and value: Singapore’s middle class pays a smaller share of income in direct taxes but receives strong public infrastructure, efficient transport systems, and reliable services. Kenya’s middle class pays a larger share of income while still spending privately on services such as security, education, and water.

Weak Points for Kenya's Taxation

Kenya’s structural pressures: The government relies heavily on the formal sector Payroll taxes become the easiest revenue source. This concentrates the tax burden on salaried workers.

Perceived double taxation: Many households pay high income tax and still face high indirect taxes, such as value-added tax at 16% and fuel levies. This creates the feeling that the same income is taxed multiple times.

Administrative complexity: Multiple mandatory schemes, such as NSSF, SHIF, and the Housing Levy, increase payroll complexity for employers and reduce transparency for employees.

Weak Points for Singapore’s Taxation

Singapore’s cost pressures: Income tax remains low, but other policy tools create high indirect costs. For example, car ownership requires a Certificate of Entitlement, which can exceed 100,000 dollars.

Consumption taxes: Singapore raised the Goods and Services Tax to 9 %. Consumption taxes tend to affect middle-income and lower-income households more than high-income groups.

High living costs: Singapore ranks among the most expensive cities in the world. Housing prices and daily living expenses absorb much of the disposable income that lower tax rates create.

Economic systems often behave like long experiments. Policy choices compound over decades. Small structural differences in taxation, savings systems, and public services slowly shape productivity, inequality, and household wealth. Over time, those quiet design decisions produce very different outcomes for citizens.

Can Kenya Build Singapore-Style Institutions?

If the Singapore comparison is to be more than political rhetorics, focus must shift to reforms that can survive political transitions.

The Bureaucracy Test: Can Kenya Build a Bureaucratic Government

Singapore’s advantage was a merit-based civil service that was stable across leadership changes. In Kenya, the civil service is often reshaped after elections.

The 2027 Question:Will any administration commit to an independent, professionally recruited, and well-paid executive cadre, legally insulated from wholesale turnover? The composition and mandate of the next Public Service Commission will be an early signal.

The Investment Test: Will “Hustler” Politics Welcome Real Capital?

Singapore attracted capital through credible, multi-decade consistency. Kenya’s climate struggles with reversals, as seen in the 2024 Finance Act protests, shifting tax positions, and the 2026 exit of Koko Networks. Koko’s departure, driven by regulatory uncertainty after capital commitment, sent a chilling signal: even high-impact businesses are not safe from abrupt policy shifts.

The 2027 Question: Can politicians present a credible, cross-party Investment Protection Pact that locks in core policies for key sectors for 10-15 years?

The “Bottom-Up” Reality Check: Informality vs. Formalization

Like Kenya today, Singapore in the 1950s and early 1960s had a large informal economy. It included unlicensed street hawkers, petty traders, casual laborers, and extensive squatter settlements. Rapid population growth, postwar disruption, and high unemployment pushed many into survivalist work outside formal regulation.

Kenya’s challenge is larger in scale. According to world banks estimates 2024 Economic Survey data, about 90% of the workforce operates informally. The politically viable path is not sudden formalization, but a phased, incentive-based strategy that could span three election cycles.

The Formalization Journey: Singapore vs. Kenya

Singapore’s transition wasn’t just about taxes; it was about licensing for dignity and space. They moved people from the streets into managed hubs, providing a clear value proposition for becoming formal.

Comparison table of Singapore’s 1950s-1980s development model versus Kenya’s 2026 socioeconomic strategy, highlighting informality, financial inclusion, enforcement, and policy challenges.

The 2027 Question: Manifestos and Scenarios

As the 2027 cycle approaches, the main tension will be between short-term populist relief and long-term structural reform. Past cycles and current economic indicators suggest three likely paths:

Scenario 1: Populist Relief (Short-Term)

Focus: Direct cash transfers, Hustler Fund top-ups without repayment conditions, and temporary fuel or maize subsidies. Outcome: Politically popular but increases national debt. It addresses poverty symptoms without formalizing informal businesses, leaving the bridge to formalization incomplete.

Scenario 2: Structural Economic Reforms

Focus: Connect the Hustler Fund and the proposed Nyota Fund to a Unified Registry. Businesses must obtain a simplified Micro-License to access higher credit limits or government contracts under the 30% AGPO rule.

Outcome: Creates incentives for formalization, similar to Singapore’s approach. The government offers benefits, cheap credit, and contracts, rather than relying solely on enforcement, enabling self-driven integration into the formal economy.

Scenario 3: Digital Tax Enforcement

Focus: Use AI and M-Pesa data to track economic activity and automate tax collection, for instance, through eTIMS for small traders.

Outcome: Likely strong resistance. Without clear benefits like better markets or healthcare, informal businesses may move entirely to cash to avoid digital tracking.

The Devolved Dimension: Can Counties Forge Their Own "Mini-Singapore" Pacts?

Singapore’s model was centralized. Kenya’s 47 counties add immense complexity. A national “Singapore Dream” must be decentralized.

The 2027 Question: Will campaign platforms include model county charters or performance-based conditional grants to incentivize county-level policy continuity, efficient revenue collection, and local investment hubs? Transforming Mombasa, Kisumu, or Eldoret into regional excellence centers may be more achievable than one national miracle.

What Singapore Had That Kenya’s Politics May Not Allow

Comparison table explaining why Singapore’s 1965-1990 development model cannot be replicated in Kenya’s 2025 political and economic context.

These contrasts show why Kenya cannot simply copy Singapore’s path. Long-term, large-scale reforms will always compete with electoral pressures, county-level demands, and public scrutiny. For the 2027 elections, this means candidates must design policies that balance ambition with political reality. Success will depend less on bold slogans and more on creating institutions, incentives, and commitments that can endure beyond a single term.

The Price of Policy Reversals

In Kenya, frequent midstream policy changes have made long-term planning difficult for both local and foreign firms. When tax policies, sector regulations, or government priorities change abruptly, investors respond by slowing down, scaling back, or exiting the markets. When rules are unstable, investors demand higher returns or redirect funds elsewhere.

Policy uncertainty carries a quantifiable cost. Abrupt changes in policies result in investors demand for risk premium. If uncertainty adds 3 to 5 % to the cost of capital in Kenya compared to more stable peers, this translates into billions of shillings in foregone investment and higher project costs over a decade. Manufacturing, infrastructure, and green energy suffer most, yet these are the sectors that create formal jobs and lift productivity.

Higher financing costs weaken public and private investment. Firms delay expansion or choose short-term projects with quick exits. Government projects become more expensive, forcing either higher borrowing or reduced scale. This dynamic worsens debt sustainability because erratic policies suppress the growth needed to service existing obligations.

Public projects are affected by political turnover. Large initiatives often span multiple terms, yet priorities shift after elections. Delays raise costs and dilute impact. By completion, conditions may have changed, and the original economic logic is weakened.

As Kenya’s 2027 elections approach, this pattern matters. Elections are not just political moments. They are economic stress tests.

Kenya’s 2027 Election Scenarios

Kenya’s 2027 election will signal which path the country prioritizes.

Scenario 1: The Reform Mandate A winner gains a mandate for institutional reform: a 10-year civil service overhaul, a bipartisan Investment Protection Pact, and legal insulation for key agencies such as KRA, National Planning, and many more. This aligns with the Singapore systems-first approach.

Scenario 2: The Populist Pivot The election is decided on short-term promises: subsidies, cash transfers, and tax reversals. Hard reforms are postponed. The Singapore vision remains a campaign slogan, not a governance plan.

Scenario 3: The Coalition Stalemate (Most Likely)

A fragmented result leads to a coalition government. This could either force a cross-party consensus on a narrow set of core reforms (a silver lining) or result in policy paralysis and populist outbidding within the coalition.

The Kenya Populist Review: Hope vs. Austerity

Kenya’s 2022 election marked a populist victory. President William Ruto shifted political focus from ethnic blocs to class dynamics, promising a Bottom-Up Economic Transformation Agenda (BETA).

The Populist Promise: Cheap credit through the Hustler Fund, lower living costs (subsidized maize), and shifting the tax burden to wealthier citizens.

The Reality Check (2024-2026): With maturing Eurobonds and a high debt-to-GDP ratio, the government reversed course. Instead of broad relief, it introduced aggressive tax hikes (Housing Levy, SHIF) and removed fuel subsidies. The middle class and informal sector the “hustlers” became the face of anti-tax protests. This illustrates the Populist Trap of promising the impossible to win elections, then enforcing austerity to prevent default.

Comparative Collapse: Why Populist Policies Fail

Populist leaders often follow a three-stage cycle: Boom (high spending), Crisis (inflation/debt), and Collapse.

Venezuela (Chavez & Maduro): Resource-based subsidies funded by oil. Oil price drops forced money printing, causing hyperinflation, resulting in a 90% poverty despite vast oil reserves.

Argentina (Kirchner Era): Nationalized industries, froze prices, and manipulated inflation. Isolation from global markets led to repeated debt defaults, resulting in 100%+ inflation and chronic instability.

Turkey (Erdoğan): Low interest rates were enforced despite inflation, resulting in a currency collapse and severe loss of middle-class purchasing power.

Greece (Syriza, Tsipras): Anti-austerity promises clashed with Eurozone rules, resulting in a forced, harsher austerity than the previous government.

Key Patterns in Populist Failures

Elite Scapegoating: Blaming external actors prevents addressing structural problems like debt or productivity. Institutional Erosion: Central banks and independent institutions are undermined in their ability to deliver short-term promises.

Subsidy Dependence: Populists rely on subsidies; their removal provokes unrest.

Short-Term Focus:Policies target the next election, not long-term infrastructure or education.

Lesson for Kenya

Kenya stands at a crossroads. The collapse of the Hustler narrative shows that populism is effective for campaigns but weak for governance. Ignoring fiscal realities in favor of popular promises risks harming the poor more than the elite, as seen in Venezuela and Argentina.

What Kenyans Should Listen to in 2027 Campaigns and Beyond

As politicians invoke the Singapore analogy, voters and investors should focus on specifics, not slogans.

● “We will amend the Constitution to…” Question: Will it create an independent Public Service Commission with secure funding and merit-based appointment powers?

● “We will pass a law that…” Question: Will it be a 15-year Industrial Stability Act that guarantees tax and regulatory terms for strategic sectors?

● “Our first budget will prioritize…” Question: Will it fund technical training and industrial infrastructure over political pet projects?

● “Our deal with counties will…” Question: Will it reward counties for long-term economic governance and local investor attraction?

The Bottom Line for Kenya in 2027 and Beyond

Kenya will never be Singapore. But it can become a more capable, predictable, and productive version of itself by building institutions that outlast governments.

The 2027 elections are a crucial test. They can either reinforce short-term cycles or create a rare consensus that the next decade must focus on building a state that delivers beyond a single term.

Kenya’s real “Singapore Miracle” would not be skyscrapers. It would be:

A competent, respected, and permanent civil service.

A bipartisan economic policy pact that survives elections.

A phased, realistic formalization strategy for the informal sector.

A decentralized model where counties compete on good governance.

That’s the transformation that will outlive a campaign promise.

Key Recommendations for Kenyans Towards 2027 and Beyond

Vote for Institutions, Not Individuals. Look for manifestos that detail laws and pacts, not just visions, to shield economic policy from future political changes.

The Bureaucracy is the First Test. A serious reformer will have a clear plan to professionalize, pay competitively, and legally protect the civil service from post-election purges.

Demand a Stability Guarantee for Investors. Promises of new projects are empty without a credible, legal commitment that tax and regulatory rules won't change midstream after the election.

Scrutinize the "Informal Sector" Plan. Reject promises of only continuous handouts. Support plans that offer a clear, incentivized pathway to formalization, with access to credit and land for registered businesses.

Calculate the Populism Premium. Every promise of abrupt policy reversal has a cost. Understand it means higher long-term interest rates, fewer stable jobs, and costlier goods.

Think 20-Year Institution, Not 5-Year Plan. The most credible candidate will be the one who talks most about limiting their own (and their successor's) power to meddle with economic fundamentals for the sake of long-term growth.

The bottom line: In 2027, the real Singapore style promise for Kenya skyscrapers, it is a system that works even when governments change.

Takeaway

Kenya’s future in achieving sustained growth depends less on political promises and more on institutional credibility. This is only possible if the country can:

strengthen governance

stabilize policy

integrate its informal economy

Frequently Asked Questions

1. Why do "Singapore-style" promises fail after elections? Debt consumes an estimated 65% of revenue. Campaign promises require spending, but reality forces tax hikes and subsidy cuts post-election.

2. Does Kenya's middle class get value for its taxes? No. They pay estimated 32% but still pay for private security, water, and schools. Singapore pays an estimated 24.5% and gets world-class public services.

3. Why do investors leave Kenya? Policy reversals. Koko Networks exited in 2026 after regulatory chaos. Each reversal adds 3-5% to Kenya's cost of capital.

4. Can devolution work with long-term planning? Yes, through "mini-Singapores." Let Mombasa (logistics) and Kisumu (agro processing) compete on governance, not wait for a national plan.

5. What's wrong with populist funds like the Hustler Fund? They follow a boom-crisis-collapse cycle. Kenya already reversed course with tax hikes. Venezuela and Argentina show the poor pay the price.